Today “work from anywhere” is a massive and growing trend, but it is a painful reality of high fees, FX, and admin for workers. Stablecoins enable global workers to be paid like a local, no matter where they live. Still, platforms have avoided going deep with Stablecoins for the additional regulatory, liquidity, and operational challenges they present to support globally.

Sardine can change this and has built the safest, fastest way to pay workers internationally.

Global workers need better global payouts

“Work from anywhere” has been life-changing for hundreds of millions of people. Talented workers in the global economy can find high-paid work from western companies, and domestic talent can live and work wherever they choose.

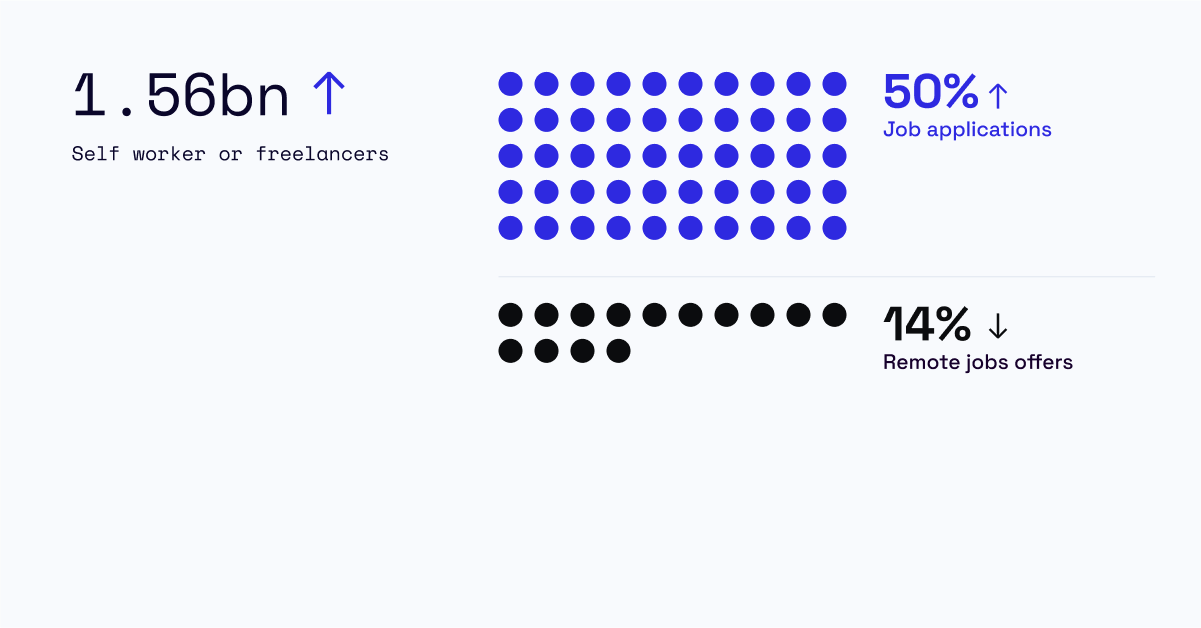

More flexible working arrangements are here to stay. 1.56bn people work as self-employed or freelancers. Statistics from LinkedIn show that despite only 14% of jobs being remote, those jobs receive 50% of applications.

If employers embrace “work from anywhere,” they benefit from a global talent pool that may be more affordable or skilled than they have in their local labor market.

The workforce for many companies is becoming default global, but the simple act of getting paid is not default global. The market needs a better solution for paying remote workers that works in any currency and don’t penalize workers for currency exchange.

Getting paid internationally is still too hard

If the worker being paid is outside the US or lives in the US and wants to remit money outside of the US, they face a series of challenges.

- Most platforms pay in dollars and leave the worker to figure out how to get those dollars into local currency to be available to spend on essentials like rent, food, and wifi.

- Many remittance solutions are expensive, meaning workers lose a portion of their paycheck to fees

- In some high-inflation markets (like Argentina), using the banking system to convert to local currency can reduce a worker’s income by up to nearly 2.5x in real terms!

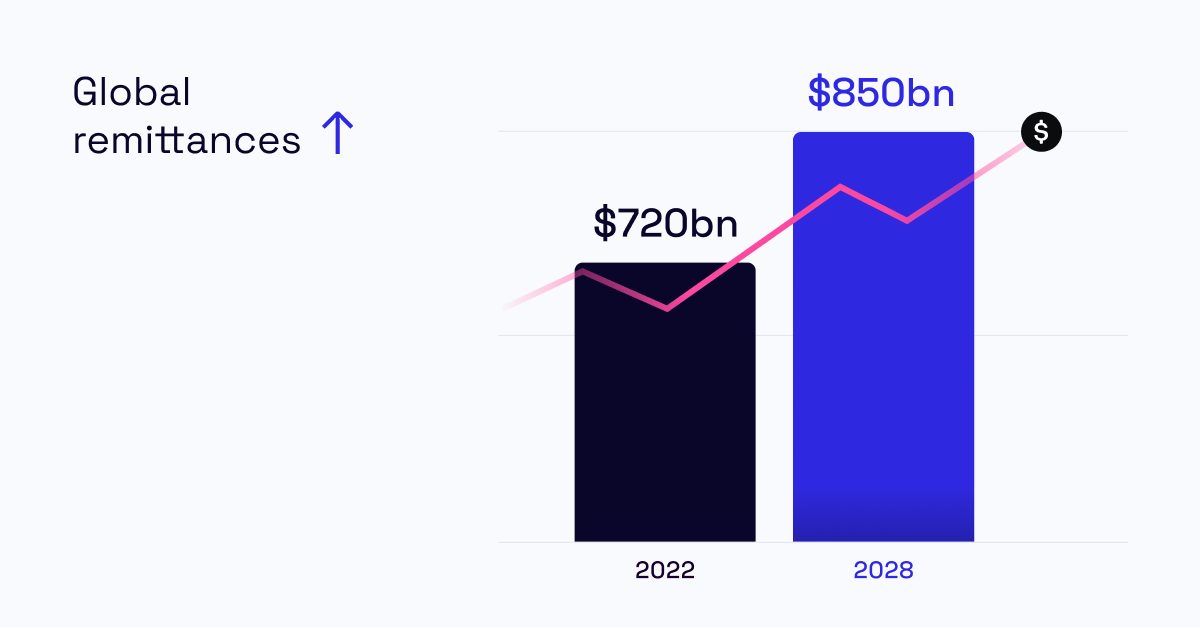

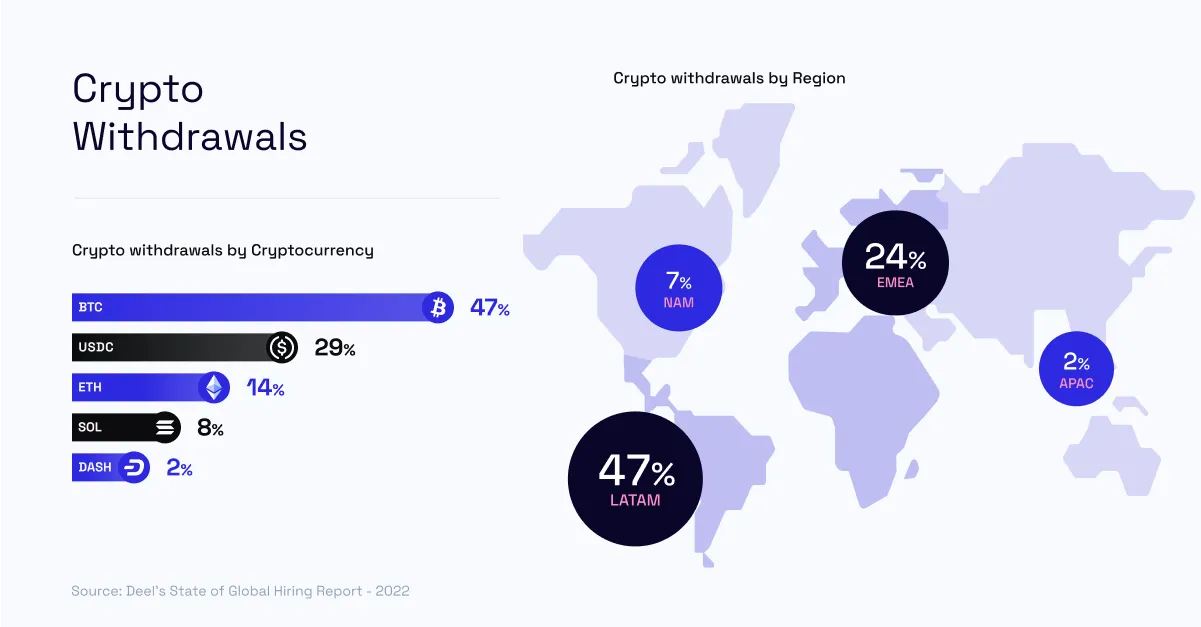

Global remittances hit $720bn in 2022 and are forecast to hit $850bn by 2028. Additionally, demand for monthly withdrawals in Crypto more than doubled over the time period from July 2021 to Jan 2022. This demand for Crypto withdrawals primarily comes from LatAm (47%) and EMEA (24%). Unlike their domestic counterparts whose paycheck lands in their account, international workers have additional admin and costs to manage.

Payroll platforms default to domestic currencies

Payroll platforms often require a traditional banking or account endpoint to pay workers. In the US context, this means having a US bank account. Their operational, regulatory, and FX exposure for platforms increase as they move into international payments.

This is challenging for the recipients to manage,

For example, suppose an Argentinian citizen gets paid by a US company.

If the company sends an international remittance through their bank to Pesos, they get only 170 pesos to the dollar, given the official exchange rate. If they were to go to a “Cueva” in the blue market — they would be getting 350 pesos to the dollar. Taking such a huge pay cut is not attractive.

This leaves two options.

- Open a US bank account as a non-us resident. This is difficult, even though perfectly legal. It can be done but it is challenging.

- Open a balance with TransferWise or Payoneer. Opening these is slightly easier; they come with a local account and routing number.

Once you have USD, you still have to spend it and use it to pay utility bills.

Again there are two legal options:

- Fly to Miami or NYC and withdraw cash from the bank account (around $10–20k). Fly back to Argentina, store it in a safe or a box, and go to the Cueva whenever exchanging it back to Pesos.

- Have a friend in the US manage the USD and convert it when they visit Argentina. The user keeps USD in a Wise or Payoneer account and sends it to a friend or someone they trust in the US, which gives the user cash in person when visiting Argentina,

But now there’s a 3rd option.

Stablecoins are cash, and the Cuevas accept Crypto.

Stablecoins present another rail

Stablecoins have the advantage of being instant, global, and 24/7.

A compatible wallet is all anyone needs to pay or get paid in Stablecoins. They can then send that “dollar” to anyone almost instantly and nearly free.

1:1 backed Stablecoins (like USDC, GUSD, and USDP) are digital representations of the US dollar held at a regulated US financial institution or equivalent. Many of the largest Stablecoin providers are audited and store customer funds in dollars or dollar equivalents. While there is some regulatory uncertainty about the treatment of these assets, they are well understood by consumers.

This has become so compelling that some international worker platforms already offer wallet integrations for Stablecoins.

Barriers to adoption for platforms

If a platform chooses to support Stablecoins (or Crypto more broadly), they would need to

- Source Stablecoin liquidity

- Ensure compliance with BSA/AML for payments to consumers

- Manage the integration to wallets.

Platforms often don’t want to store and manage Crypto; their default motion is to pay a bank account, which is also compliant with the Bank Secrecy Act (BSA) and Anti Money Laundering (AML) laws and rules. A regulated direct deposit account is subject to these checks within the US (as are its equivalents internationally).

A platform could be available to most Stablecoin-compatible wallets with relatively low lift integrations. Still, in doing so, they’d have to KYC each customer and take on the legal risk of paying someone in stablecoin rather than local currency.

Perhaps its time for a new approach.

A critical way to manage the risks associated with Stablecoins is to ensure all workers open a direct deposit account in their name in the US. The employer of record can then pay their workers exactly as they do today.

Many international workers don’t have a US account, and those that do might prefer the seamless transfer and better rates afforded by Stablecoin payouts.

What if we could offer a best-of-both-worlds scenario to platforms and workers?

Platforms pay the worker just as they would today to a bank account. It’s entirely possible if we can instantly remit money globally via Stablecoins. We need better on-ramps and off-ramps, and with all these things, the hardest part is managing compliance and edge cases.

Fortunately, that’s what we’re great at.

If you want to make payroll safer and faster, get in touch.