Crypto and Fintech wallets have suffered high decline rates in wallet funding. In Crypto wallets, Sardine market data shows an average 55% decline rate (ranging from 26% to 71%). For businesses that rely on wallet funding, turning away 1 in 2 customers impedes long-term growth. Customers that are rejected often never return. By contrast, Sardine customers using bank funding average 95% approval rates (with a high of 98%).

The causes of high decline rates

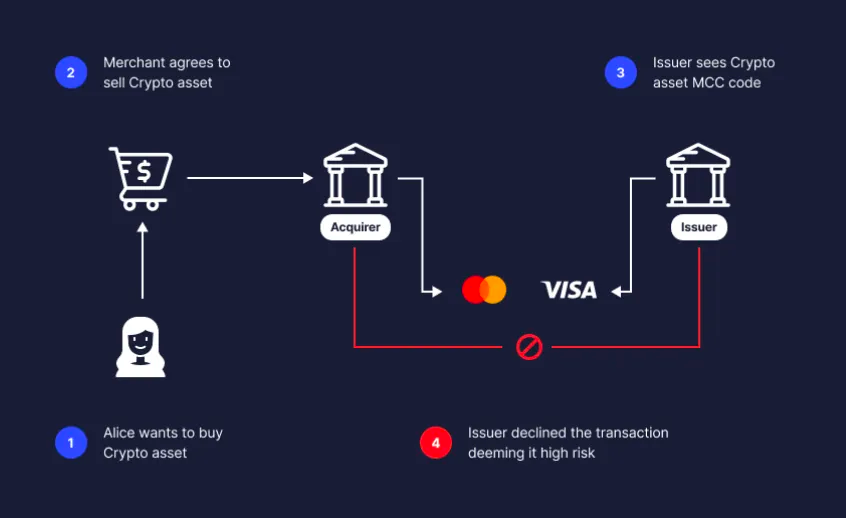

The consumer using their debit or credit card is often declined by their card issuer (the bank or account provider they’re using to fund the wallet). The card issuer is declining because they view transactions to a Fintech or Crypto wallet as a high fraud risk.

Card issuers have a sophisticated risk model which determines whether a transaction would be approved or not. 2 of the major inputs in it are

- Merchant’s existing or past fraud rates and

- The riskiness of the merchant category code

1. Fintech wallets and Crypto businesses have been targeted by fraudsters, especially during the pandemic, as they grew significantly in popularity.

- According to Aite-Novarica Group, Fintechs have an average fraud rate of around 0.30%, double that of credit cards that average of 0.15–0.20%.

- In 2021, $1.46bn was lost to Crypto Investment scams targeting the over 60s (this more than doubled between 2020 and 2021 according to the FTC).

- Fraudsters will also use non-compliant Crypto exchanges to hide fraud proceeds before attempting to collect in legitimate wallets.

2. These merchants have their own merchant category code (MCC Code). A merchant category code is how banks and other card issuers identify the type of merchant trying to pull money from one of their customer accounts. Based on this code, card issuers may decline the transaction if it is high risk.

The code that Fintech and Crypto businesses fall into is considered high risk.

6501: Non — Financial Institutions — Foreign Currency, Money Orders (not wire transfer) and Travelers Cheques and other similar services)

The card issuers will use the MCC Code as one signal, but they’ll also look at the fraud rates they get from a specific merchant. So if they see a merchant in a high-risk MCC code, the card issuer might monitor that merchant over time. If the merchant demonstrates low fraud rates, their approval rates will improve.

While Sardine has worked with numerous clients to improve their card decline rates by reducing fraud, experience has also shown there’s also a valuable alternative; bank funding.

Bank Funding: An alternative to cards for wallet funding

In bank funding, a consumer can directly load funds into the wallet by entering a receiving bank account number and using bill payment rails (Like ACH in the US or SEPA in Europe). Sardine customers using bank funding saw higher approval rates (avg 95% vs. 55%) and a higher average transaction amount (avg $480 vs. $221).

Crucially, the merchant and not the bank (or issuer in card terminology) make the decision or approval. The merchant has more control. This is why Neobanks in the US have built ACH integrations for wallet funding.

So why isn’t everyone using bank funding for crypto wallet loads?

- Settlement delays

- High fraud rates

Settlement delays

Decades of e-commerce have shown that instant and responsive checkout and conversion experiences are critical for both consumers and businesses.

The most common form of bank funding in the US, ACH, has a 2-day settlement delay. For a consumer funding their wallet, this can lead to a nervous wait and create a lack of engagement for wallets. And especially with crypto, most users want to engage in DeFi, or buy NFTs with the crypto instantly. Hence instant funding of your wallet is critical for a seamless user experience.

Managing fraud is critical

With higher funding amounts often comes higher fraud risk; indeed, Sardine’s data shows that the average fraud loss in account funding is higher than in cards ($1,050 vs. $350). Fraudsters will often target instant funding sources because they can quickly use or move the money once it is loaded into a wallet.

Because the merchant is liable for the fraud, any fraud losses must be covered by the merchant. If a consumer reports fraud to their bank, and the bank agrees there is fraud, they can claw back the original purchase amount. This can represent significant lost revenue to merchants.

To fund a wallet with account funding, a business needs to be very confident before it moves the money.

But merchants can manage settlement delays and fraud.

Overcoming settlement delays with Risk-free Instant settlement

One innovative solution for the two-day settlement delay used by many wallets is to pre-fund a customer’s wallet while waiting for the funds to arrive from their bank account. An instant settlement requires understanding the customer risk, which often involves setting a limit per customer (e.g., $500) to avoid the significant fraud losses. However, this breaks one of the key benefits of bank funding, the higher limits.

To create the best customer experience, wallets need instant funding.

To get higher limits, wallets need the best fraud prevention and detection.

Detect & prevent account funding fraud

Preventing, detecting, and then managing fraud has no one size fits all solution, but there are several steps merchants can take to reduce fraud rates dramatically.

- Asking for customer validation (e.g., micro-deposits to prove the consumer is who they say they are, or asking the customer to log in to their bank via a service like MX or Plaid)

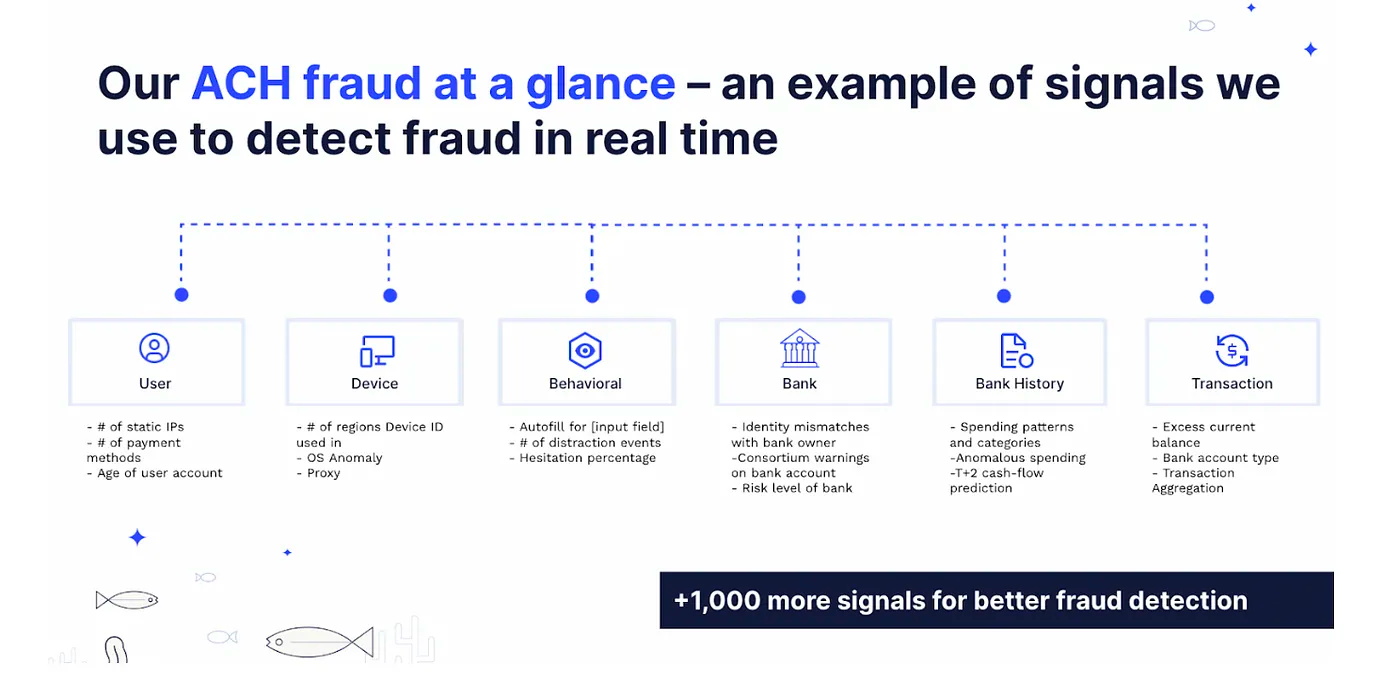

- Understanding the user and their device (e.g., Is the user typing as they normally would? Is the user suddenly using a new device? Are they using IP ranges familiar for them? Is there a proxy or VPN being used? Is remote desktop software being used?). There are 1,000s of possible behavior and device signals (even ones you wouldn’t expect, like the device audio setup, and orientation).

- Understanding the transaction (e.g., Is this transaction unusually high for this user? Is this the right time of day for the user?)

- Accessing databases about users and devices. (e.g., Has this email address or SSN been compromised in a hack? Has a bank seen fraud from this account? Has the device had its SIM swapped recently?)

The more data a merchant can gather about the user and their device, the more sophisticated they can become at fraud prevention.

(The mighty Zahid will have a blog post coming soon specifically focused on how to prevent fraud in ACH, so look out for that!)

Choosing the right funding method

Ultimately consumer choice is critical, and cards are a widely accepted service with built-in customer protections. But providing the consumer with more choice and potentially a better experience is worth exploring.

Some Neobanks chose ACH funding because of its control over the experience. At Sardine, we believe this will become the default method for wallet funding and Crypto purchases in the US rather than cards based on cost and conversion rates.

If you want to learn more about how Sardine provides instant settlement and prevents fraud with higher limits and approval rates, contact us.