Financial crime doesn’t happen in silos, but too often our defenses still do.

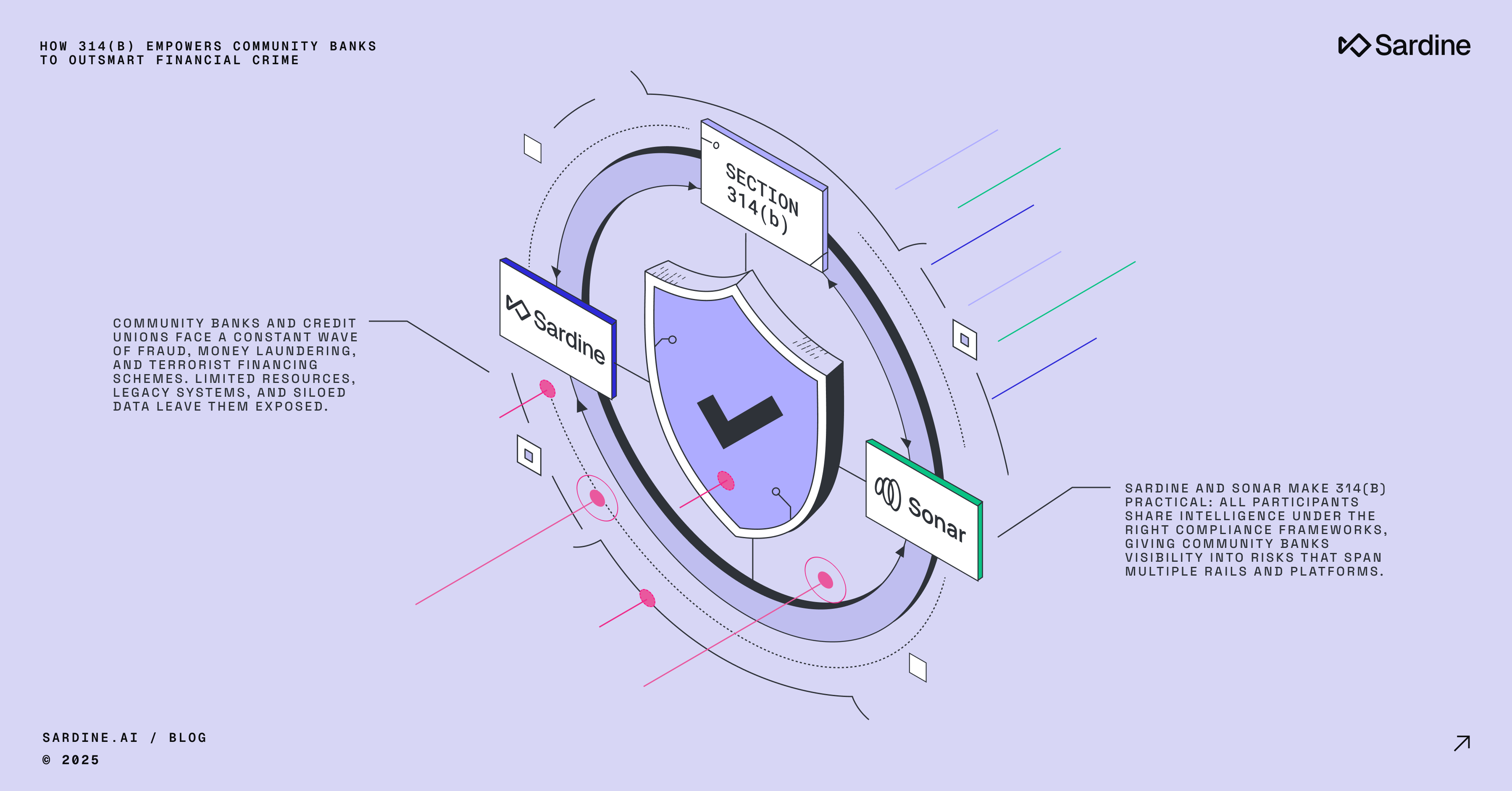

Across the U.S., community banks and credit unions face a constant wave of fraud, money laundering, and terrorist financing schemes. Limited resources, legacy systems, and siloed data leave them exposed. Criminals exploit those gaps by spreading activity across multiple institutions, layering transactions, and hiding in the noise of legitimate customer behavior.

No single institution can see the full picture anymore. The threats are too networked, the rings are too agile, and the data is too fragmented.

That’s why Section 314(b) of the USA PATRIOT Act matters. It gives banks and credit unions a legal framework to share information with each other to uncover criminal networks that would otherwise remain hidden. When institutions connect the dots across their customer activity, what looks like a minor anomaly becomes part of a much larger pattern of crime.

Why 314(b) is more than a compliance exercise

314(b) was designed to enable collaboration. It allows institutions to legally share intelligence and reveal risks no one bank could uncover alone. FinCEN has called it “critical to protecting national security.” For community banks and credit unions, where visibility is often limited to internal systems, 314(b) is a way to see the bigger picture:

Reveal complex money trails

A community bank notices a customer making regular cash deposits followed by quick wire transfers overseas. On its own, the behavior seems minor. But when shared under 314(b), another bank reports the same individual is using different aliases to move funds in the same pattern. Together, the activity reveals a coordinated laundering scheme no single bank could have spotted.

Complete the customer picture

A credit union sees slightly unusual ACH activity but lacks enough context to escalate. Through 314(b) sharing, another institution confirms the same customer was flagged for suspected PPP loan fraud. Combined, the insights show clear risk and allow the credit union to take action.

Early detection of financial crime

A regional bank identifies a mule account pattern and shares device and user data under 314(b). Days later, a credit union sees the same device fingerprint during a new account application. The early warning lets them block the account before fraud can occur.

File richer Suspicious Activity Reports (SARs)

Instead of filing a general SAR based only on limited observations, a bank gathers supporting information from two other institutions using 314(b). The combined data creates a clear story of transactions, entities, and behaviors. The resulting SAR gives law enforcement a stronger lead and accelerates the investigation.

Why your current fraud and AML stack isn’t enough

Most fraud and AML systems in use today were built for a slower era of banking. They rely on static rules, siloed data, and manual reviews. That design leaves community banks with only a partial view of customer and transaction risk, while criminals take advantage of the blind spots by spreading activity across institutions.

The result is fragmentation at every level:

- Solution fragmentation: Transaction monitoring, sanctions screening, onboarding, and fraud prevention often run on separate tools. Investigators are forced to stitch cases together across platforms, slowing them down and leaving gaps.

- Data fragmentation: Customer information is scattered across disconnected systems, so there is no single source of truth.

- Split view of entity risk: Fraud and AML systems often assess the same individual differently, leading to duplicate alerts, missed patterns, and inconsistent outcomes.

- Partial view of customer behavior: A bank can only see what happens within its own walls. Without visibility into activity across other institutions, critical risk signals stay hidden.

Even with the best internal data and third-party feeds, the view remains incomplete. A single institution cannot see how an entity behaves across the wider financial system. That is why criminals can move freely between community banks and credit unions without detection.

Collaboration changes that equation. When banks share intelligence under 314(b), they expose the networked behaviors that fraud and AML systems alone will always miss. What looks like an isolated anomaly in one institution can reveal a coordinated scheme when seen across many. Without that collaboration, false positives keep piling up, real threats slip through, and institutions remain exposed.

Protect your bank by collaborating with other institutions

Community banks and credit unions remain central to the health of the U.S. economy, which is why criminals target them. Fraud rings and laundering networks know that smaller institutions often have fewer resources and narrower visibility.

314(b) provides a way forward. By working together, banks and credit unions can move from isolated defenses to shared intelligence that strengthens everyone. Collaboration under 314(b) helps institutions:

- Strengthen defenses by extending visibility beyond their own walls and identifying risks that no single bank can spot alone.

- Protect customers and communities by intervening earlier to stop exploitation before losses mount.

- Reinforce trust and regulatory confidence by demonstrating that compliance is handled with rigor and foresight, not just obligation.

Most institutions want to collaborate but struggle to do it securely, consistently, and at scale. That is where the right technology becomes critical, turning 314(b) from a regulatory allowance into an operational advantage.

How Sardine and Sonar make 314(b) practical

Most banks see the value of 314(b) but struggle with the logistics. Sharing information securely, keeping records, and making collaboration part of day-to-day investigations is hard to do with manual processes or legacy systems.

Sardine enables investigators to collaborate with other 314(b)-eligible institutions directly within the dashboard. Case details, entity information, and supporting evidence can be exchanged in a compliant way, without adding new workflows or tools. That turns 314(b) from a theoretical option into something that fits naturally into existing investigations.

Sonar extends that collaboration across the financial ecosystem. It brings together not only banks and credit unions, but also fintechs, payment processors, card networks, and crypto platforms. All participants share intelligence under the right compliance frameworks, giving community banks visibility into risks that span multiple rails and platforms. What once looked like isolated activity at a single bank can now be seen as a part of a broader pattern of fraud or laundering.

If you’d like to see how your bank can use Sardine and Sonar to strengthen collaboration under 314(b), contact us for a demo.

And if you’d like to take the next step in collective defense, join the Sonar consortium and gain visibility into risks before they reach your walls.