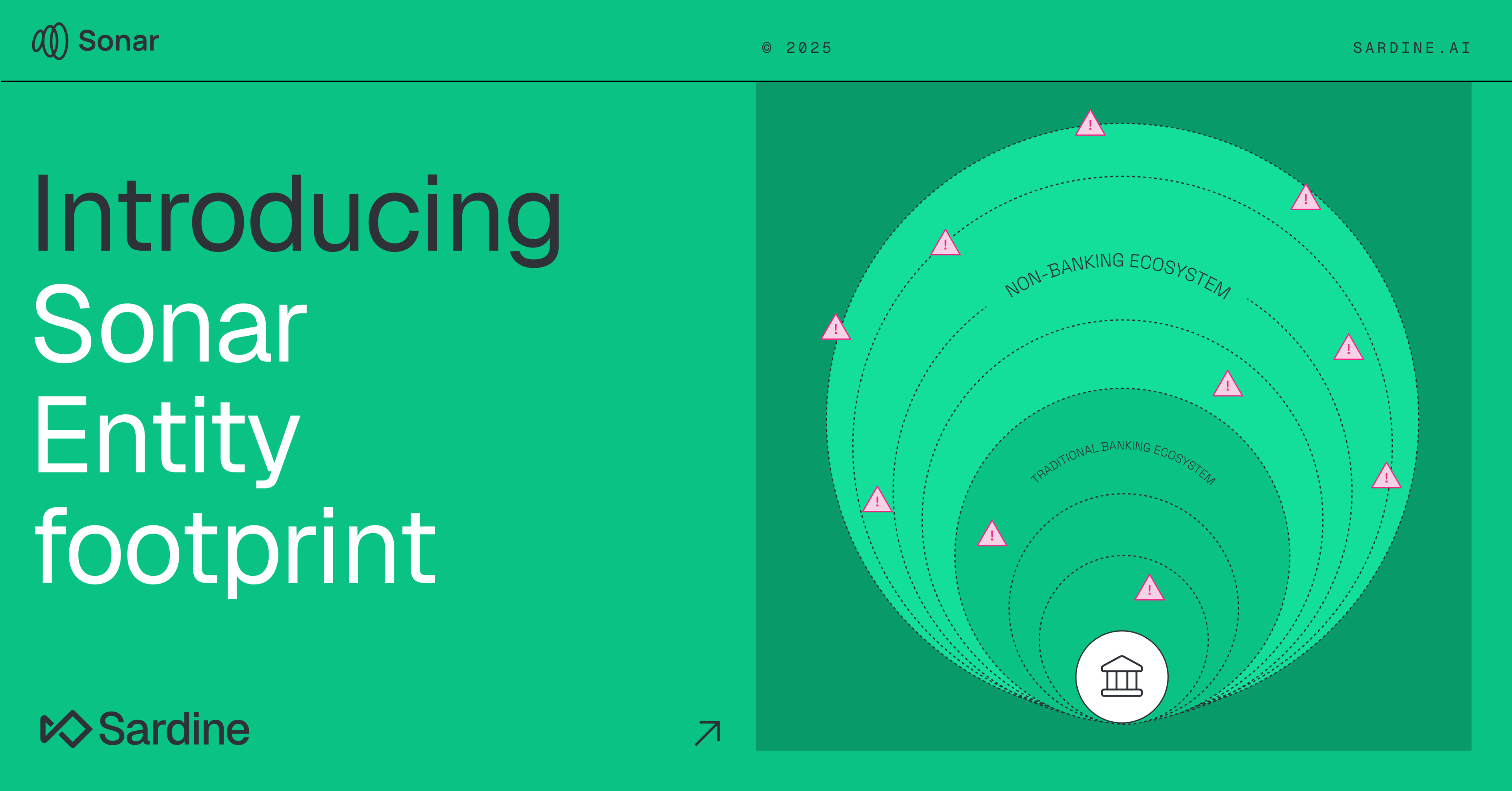

Banks have traditionally assessed risk through the lens of banking data such as deposits, credit files, transactions, and account history. But now, activity across fintechs, crypto, remittance apps, and online marketplaces plays an equally important role in understanding entity risk. Without entity risk visibility into those ecosystems, banks miss early warning signs of fraud or mule activity until it’s too late.

Today we’re introducing Sonar Entity Footprint, a new data pack that closes that visibility gap. Entity Footprint enriches existing risk assessments with cross-industry intelligence, mapping how an entity behaves across both financial and non-financial networks including fintechs, crypto, neobanks, remittance, gift cards, and marketplaces.

By combining this external view with existing risk models and internal data, Entity Footprint gives banks a more complete entity risk assessment of who they’re evaluating and where potential exposure lies. The result is earlier detection of hidden fraud exposure, stronger onboarding and funding decisions, and portfolio-level risk visibility across the customer base.

The entity risk visibility gap

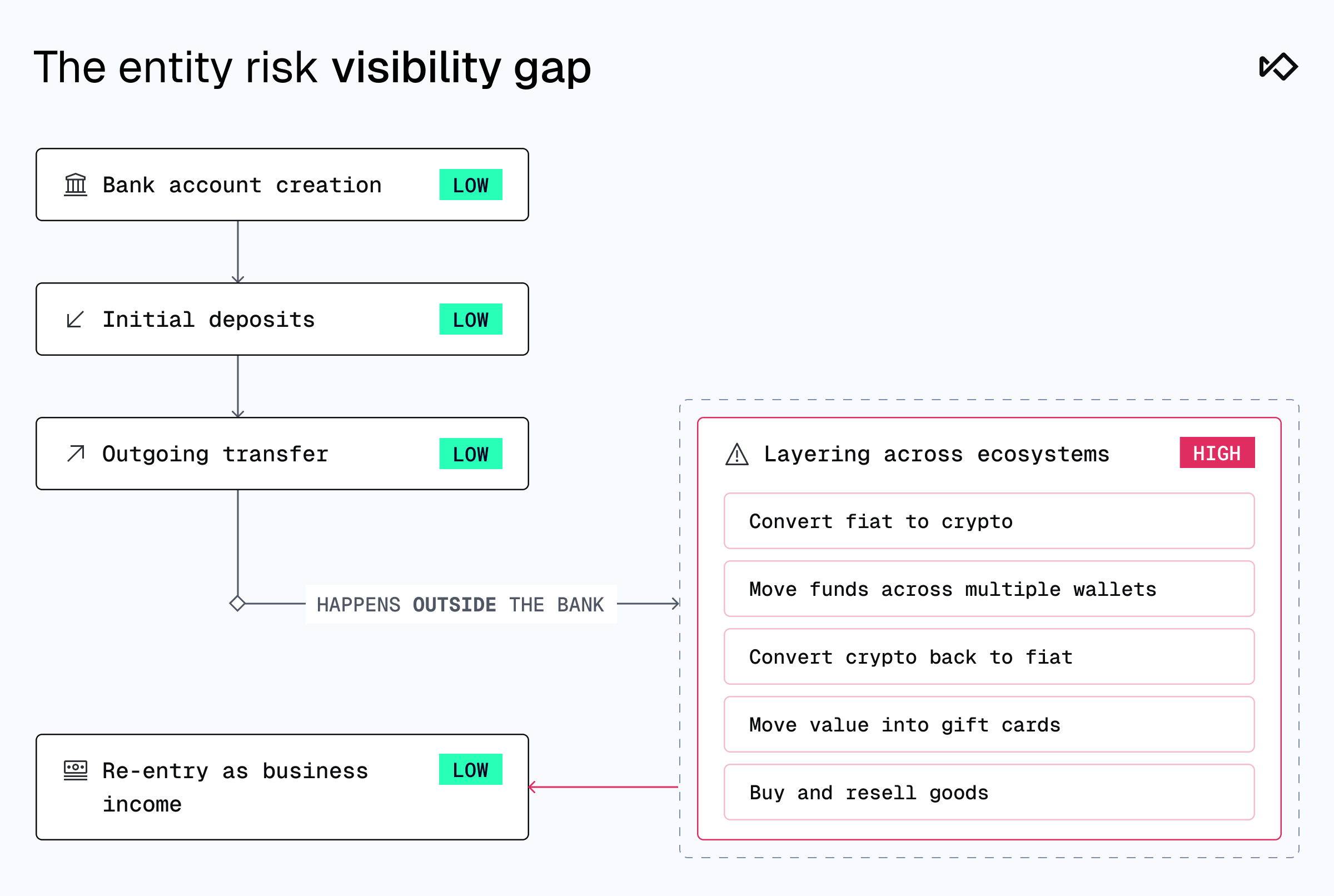

When banks onboard a customer, accept funds into an account, or investigate a transaction, they rely on what they can see in their own data such as balances, transfers, account activity, and device information. But that view only reflects what happens inside the institution.

But much of an entity’s financial activity now happens outside traditional banking channels. Bad actors move money fluidly between fintechs, crypto wallets, remittance apps, and online marketplaces. They exploit money mule risk signals, open and abandon accounts, and launder funds across channels that most banks can't see. On the surface, an entity can look legitimate in your system while showing clear red flags in other ecosystems. Without visibility into that activity, banks are left with an incomplete view of risk.

Even if a user isn’t fraudulent, activity outside of banking can reveal important signals for credit and lending decisions.Crypto entity risk signals such as leveraged positions, high balances on BNPL platforms, or overextension on sports betting platforms help gauge financial stability, adjust exposure limits, and support more accurate underwriting decisions.

How Sonar Entity Footprint works

Sonar operates as an inquiry and response network that gives banks a simple, low-lift way to request risk insights on any entity via API. It complements your existing risk systems, so you can ingest entity risk data without having to re-engineer your risk infrastructure.

Here’s how it works:

- Inquiry: Your team submits the request using basic identifiers for a person or business, such as name, email, phone, or account details.

- Entity resolution: Sonar matches those identifiers across multiple data sources and returns a confidence score that indicates how certain the match is.

- Footprint enrichment: Once resolved, Entity Footprint adds layered intelligence from Sonar, Sardine, and selected third-party partners. Coverage spans crypto apps, gift card and prepaid platforms, automotive marketplaces, ticketing apps, sneaker marketplaces, fintechs and neobanks, remittance services, and wealth management platforms.

- Response delivery: The system returns structured insights through API with context on relevant patterns, such as rapid account creation across platforms, repeated funding activity tied to known mule networks, or unusual velocity of wallet movement.

Applying Entity Footprint in your risk workflows

Entity Footprint signals can be used across the customer lifecycle to strengthen decisions for several use cases:

- Onboarding: Identify applicants linked to mule networks or known fraud activity in other ecosystems before approval.

- Account funding risk analysis: Flag whether incoming funds originate from high-risk or previously compromised sources.

- Transaction reviews: Assess counterparties and uncover hidden exposure across payment rails, including ACH, wires, real-time payments, and crypto.

- Credit underwriting: Strengthen decisioning on thin-file or borderline applicants with external behavioral context.

- AML case enrichment: Use cross-ecosystem AML signals to correlate activity and confirm whether a flagged entity appears in other high-risk networks.

Expand risk visibility with Sonar Entity Footprint

Traditional banking data only tells part of the story. With Sonar Entity Footprint, banks can see beyond their own walls to identify risks earlier, validate customers with more confidence, and make faster, more accurate risk decisions.

If your institution is looking to strengthen risk visibility without adding complexity, Sonar Entity Footprint is built for that. It’s fully compliant with GLBA and 314(b) frameworks, enabling secure data sharing and intelligence exchange across institutions.

Contact our team to see how you can start leveraging cross-industry intelligence in your existing workflows. And if you’re interested in learning more about Sonar, visit joinsonar.com.

FAQs

What is entity risk intelligence?

Entity risk intelligence is the practice of scoring a person, business, device, or wallet against cross-institution signals (mule history, account takeover markers, shell company indicators, sanctioned-entity proximity) in real time. Sonar Footprint is Sardine's implementation.

How is entity risk intelligence different from credit bureau data?

Credit bureaus surface credit history. Entity risk intelligence surfaces fraud and AML signals: mule networks, account takeover, shell company chains, real-time pattern matches. Different problem, different data.

Is cross-institution entity data sharing legal under GLBA and 314(b)?

Yes. Section 314(b) of the USA PATRIOT Act authorizes financial institutions to share fraud and money-laundering signals with safe-harbor protection. The Sonar consortium operates inside that framework with no raw PII crossing institution lines.

What latency does entity risk intelligence add to my onboarding flow?

Sub-50 milliseconds at the 95th percentile. Sonar Entity Footprint signals are pre-scored and served alongside the standard identity verification response, so the customer sees no friction unless the score crosses the risk threshold.

What signal coverage does Sonar Entity Footprint provide?

Identity resolution across email, phone, document, device, IP, and behavioral biometrics. Plus mule-network markers, account takeover history, shell company graph proximity, sanctioned-entity proximity, and pattern matches across the consortium.