I just got back from visiting family and friends in Buenos Aires, and for the first time, I experienced something I didn't expect: being completely cashless in Argentina felt normal.

This wasn't the case even in late 2024. But on this trip? A debit or credit card or a QR payment through any bank covered me 99% of the time. Even waiters at restaurants had started keeping a second POS terminal just for tips.

It's a remarkable shift for a country that has historically had a complicated relationship with digital payments, driven by inflation, currency controls, and deep distrust of financial institutions. So what changed?

Then (pre-2023) | Now (2026) |

Cash-dominant, even in cities | 99% coverage with card or QR |

MercadoPago dominated via same-app speed | Full interoperability across all banks and wallets |

Parallel FX market (cuevas) often necessary | App-based FX increasingly viable |

Digital payments largely a Buenos Aires story | QR adoption reaches villages of 1,000 people |

The payments transformation

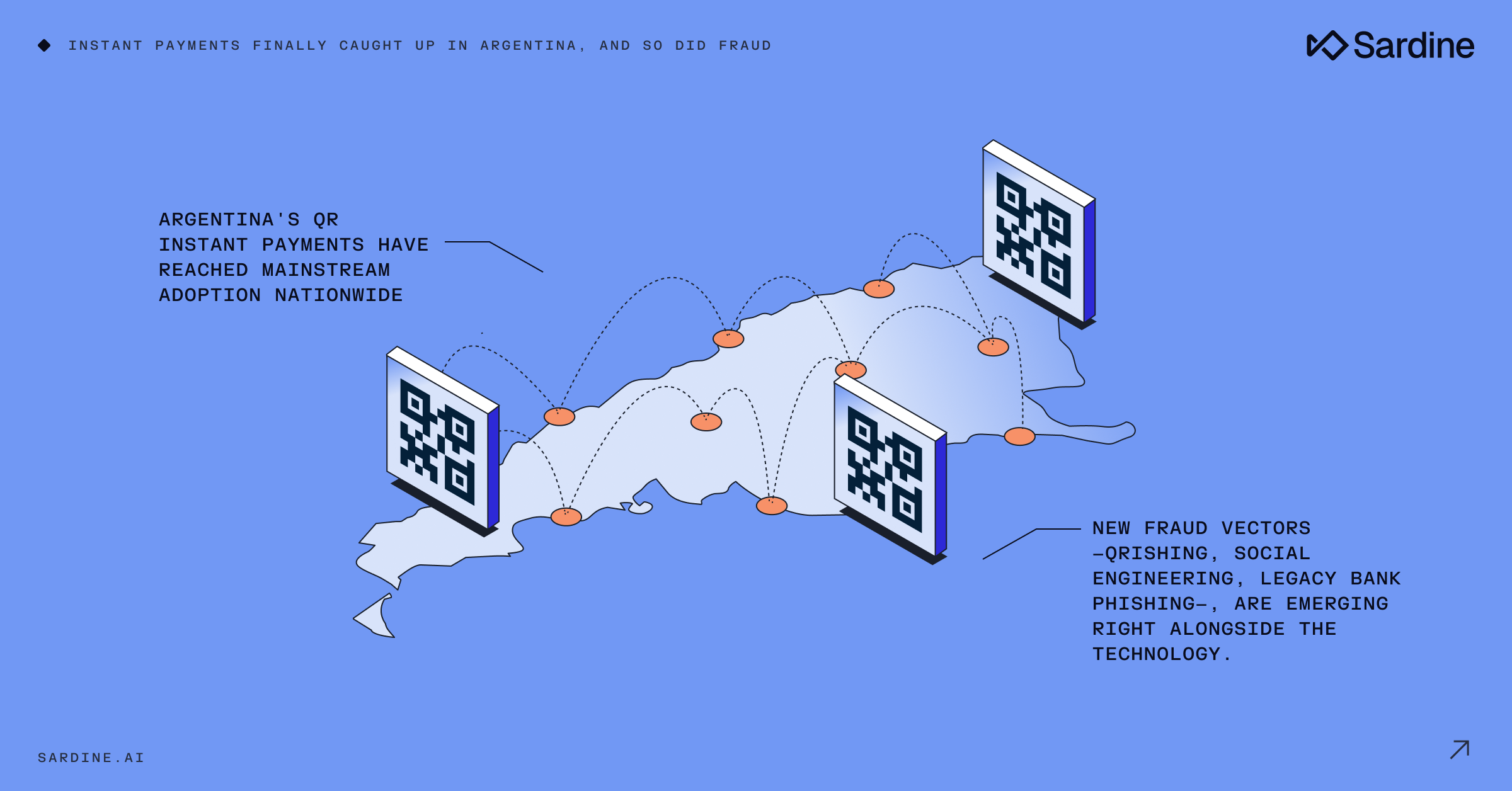

Instant payments finally have their PIX moment

The Central Bank of Argentina’s (BCRA) Transferencias 3.0 via QR has matured into something genuinely seamless, and comparable to PIX in Brazil. The days of Mercado Pago's dominance purely because same-app transfers were faster are largely over. The playing field has leveled.

My one wish: evolve the current CVU/alias key logic to support phone number, email, or tax ID lookups, the way it works in São Paulo. (I say this only out of jealousy. Someone already claimed the three-word alias I wanted. Porteños entenderán.) Transferencias 3.0 went live in late 2020 and became fully interoperable by late 2021, when all QR codes were required to work across banks and wallets. The scheme standardized rails for immediate transfers between any bank or virtual account, with funds credited in under 15 seconds, 24x7, via QR, payment links, or other identifiers. Conceptually, it’s much closer to Brazil’s PIX than to legacy card rails, as its low‑cost, irrevocable, account‑to‑account, and explicitly designed as a cash replacement.

By the end of 2023, electronic payments in Argentina grew 68% year‑on‑year, with real‑time rails such as Transferencias 3.0 representing about 36-37% of all transactions.

Analysts estimate that Argentina’s payments market was around USD $113 billion in 2025, with forecasts that it could exceed USD $500 billion by the early 2030s as digital wallets and account‑to‑account transfers grow at over 30% annually.

While PIX still leads Latin America in sheer volume, Argentina is one of the few markets that has replicated a similar blueprint: real‑time rails, universal QR interoperability, and strong regulatory sponsorship, positioning Transferencias 3.0 as a genuine regional peer.

Why Argentina's blue dollar cuevas are losing their edge (for now)

For the first time in a long while, Argentina’s parallel FX ecosystem, or the informal cuevas and street‑side arbolitos that quote the ‘blue dollar,’ just wasn’t attractive compared to the rates and convenience I could get through regulated digital channels. I bought ARS with BRL at a decent rate instantly through AstroPay without thinking twice. Meanwhile, Argentine friends visiting Florianópolis were paying at Decathlon by scanning Pix QRs through Mercado Pago, instead of bothering with dedicated cross‑border apps like belo or Cocos.

Argentina’s parallel FX market (the “blue dollar” cuevas and street‑side arbolitos) historically thrived on a wide spread between the official rate and market expectations, plus tight capital controls that limited access to foreign currency through formal channels. In that environment, cash exchanges in informal micro‑FX networks were often the only way for locals and visitors to get a realistic rate or move value quickly out of pesos.

Starting in late 2023 and throughout 2024, Argentina's government introduced an aggressive stabilization program that combined a large initial devaluation of the official peso with tightened fiscal policy and a gradual roadmap to unwind capital controls. The immediate effect was to narrow the gap between the official and parallel rates and make regulated, app‑based FX channels (like fintech wallets and cross‑border payment providers) relatively more attractive, especially for day‑to‑day spending rather than long‑term capital flight. That shows up on the ground as more people comfortable using wallets that route via Brazil's PIX, multi‑currency fintechs, or local A2A rails instead of lining up at a cueva for every trip or large purchase.

Beyond Buenos Aires: National QR and wallet penetration

This is the part that genuinely surprised me. I wasn't just paying with QR codes at porteño restaurants. I was scanning codes to buy salamines de campo (country sausages) and alfajores artesanales (sandwich cookies) in a village of 1,000 people in a southern Buenos Aires province. Some small shops were even offering a 10% discount for QR or cash payments over card, a telling sign of just how much merchants want to avoid credit card fees, and how normalized wallet payments have become even at the hyperlocal level.

That kind of geographic depth signals something real. This isn't a capital-city fintech story anymore.

Regulators and market researchers now frame Argentina’s payments shift as a structural, country‑wide transformation rather than a Buenos Aires‑only story. The central bank’s financial inclusion initiatives, coupled with Transferencias 3.0, explicitly targeted small merchants and previously underserved regions, making interoperable QR acceptance feasible even for micro‑businesses and rural retailers. Industry data shows that electronic payments in Argentina grew around 68% year‑on‑year by the end of 2023, with digital wallets capturing about a third of e‑commerce spend and nearly a fifth of POS spend, and poised to become the dominant method by mid‑decade, particularly in areas underserved by traditional bank branches.

That matters geographically: digital and mobile payments are now the fastest‑growing segment in the entire Argentine payments market, driven by smartphone penetration, aggressive fintech expansion, and the ubiquity of QR codes at small merchants.

One market forecast estimates that Argentina’s payments market will grow from about USD $86.9 billion in 2024 to roughly USD $500 billion by 2032, with digital wallets and QR‑enabled, account‑to‑account payments driving much of that expansion in both e‑commerce and point‑of‑sale transactions.

Put simply, what you experienced buying artisanal goods in a village of 1,000 people is exactly what the macro data says should be happening.

The flip side: Fraud came along for the ride

As technology progresses, inherent risks grow right alongside it. The early adoption phase is always the most chaotic, and Argentina is squarely in that phase right now.

Financial crime in Argentina isn't near the level of organization seen in Brazil, where gangs like the PCC have been known to acquire fintechs outright to launder money. But the fraud vectors I heard about on this trip were worrying in their own right.

Brazil’s organized financial crime context

In Brazil, organized crime groups such as the Primeiro Comando da Capital (PCC) have been explicitly linked to large‑scale financial crime, including bank robberies, cyber‑enabled fraud, and sophisticated money‑laundering schemes that piggyback on fintech infrastructure. Public reporting and supervisory opinions describe how mule networks, shell entities, and even regulated intermediaries can be co‑opted to funnel scam and fraud proceeds through real‑time payment systems. That’s the backdrop for frequent headlines about fraud rings exploiting PIX, and for Brazil’s relatively aggressive stance on real‑time fraud controls, industry‑wide data sharing, and mule‑account crackdowns.

Against that benchmark, Argentina’s fraud landscape is still more fragmented and opportunistic than cartel‑industrial, but the region‑wide pattern is clear: as instant payments scale, organized groups move from simple card‑present fraud into real‑time account-to-account scams, social engineering, and account‑takeover attacks, using the same infrastructures regulators built to promote financial inclusion.

Legacy banking vulnerabilities

A friend of my parents received a phishing email disguised as a web banking notification. Credentials were stolen and their checking account was wiped in minutes, with no mobile banking token ever requested. There's a significant authentication gap that legacy banks in Argentina need to close, fast.

Social engineering at the point of payment

An older acquaintance was scammed while trying to pay for a bus ride with a QR code. Someone behind her in line offered to help and ended up quietly diverting money from her mobile app. This isn't a technology failure. It's a social engineering attack exploiting user unfamiliarity with new payment flows, and it maps directly to what the industry knows about specific demographics being more vulnerable to specific fraud vectors.

Quishing and QR fraud trends

Perhaps the most concerning trend: malicious QR codes being placed over legitimate ones on transit infraction notices, restaurant tables, even parking meters. Victims scan what looks like an official payment code and their money goes elsewhere.

Globally, QR‑based fraud (“quishing” or “qrishing”) has accelerated alongside QR payment adoption. Security analyses in 2024–2025 describe quishing as an evolution of classic phishing: malicious URLs are embedded in QR codes, often delivered via email, messaging apps, printed stickers, or overlays on legitimate QR codes at restaurants, parking meters, and transit systems. Once scanned, victims are steered to credential‑harvesting pages, malware sites, or fake payment interfaces that can either drain funds directly or set up future account takeover.

Market research estimates that the global QR ecosystem, including QR codes and QR‑based payments, will grow at roughly the high‑teens to around 20% compound annual growth through 2030.

As a direct corollary, regulators and industry bodies now flag QR payment fraud as a “new type of payment fraud” that warrants real‑time transaction monitoring, URL inspection, device fingerprinting, and consumer education as key mitigants.

For an Argentina‑specific narrative, you can credibly argue that malicious QR overlays on fines, parking, or restaurant tables are the local flavor of a global quishing trend that will only intensify as QR becomes the default payment interface.

Fraud vector | How it works | Who’s most at risk |

Phishing/account takeover | Fake bank notification emails steal credentials, account drained before any token is triggered | Legacy bank customers |

Social engineering | Scammers poses as a helpful bystander at point of payment, diverts funds via mobile app | Older or les digitally familiar users |

Quishing | Malicious QR codes placed over legitimate ones on fines, restaurant tables, parking meters | Anyone paying via QR in public spaces |

What this means

Argentina's payments leap is real, and it's worth recognizing. In the span of a few years, a country that ran largely on cash and struggled with parallel exchange markets has built QR instant payment infrastructure that functions at a national scale.

But every technology adoption curve has a fraud curve that follows it. The question isn't whether fraud will emerge, it's whether the institutions, fintechs, and fraud teams building in this market are ready to respond.

The vectors showing up in Argentina right now aren't unique. They're the same playbook applied to a new payment surface. And that's actually good news: the fraud industry has seen this before, and there are playbooks for responding.

The results will speak for themselves. But the window to get ahead of this is now.