For decades card issuers, banks, and Neobanks have been flying blind in their battle against fraud, resulting in lost revenue from false declines. The data they use is often confusing and means good customers get blocked, and fraudsters get away with their crimes. The fraud squad relies on ancient formats like ISO8583 messages and NAICS codes with card transaction data.

That changes today.

Sardine and Spade are partnering to bring transparency to issuers and processors, transactions, and devices so conversion at checkout improves and chargeback rates are crushed. The secret is how Spade’s merchant intelligence, with Sardine’s brain 🧠 operating system, brings a much higher resolution to the transaction.

20/20 vision for Merchant POS Data

For card issuers like banks and Neobanks, merchant data was always unreliable and blurry.

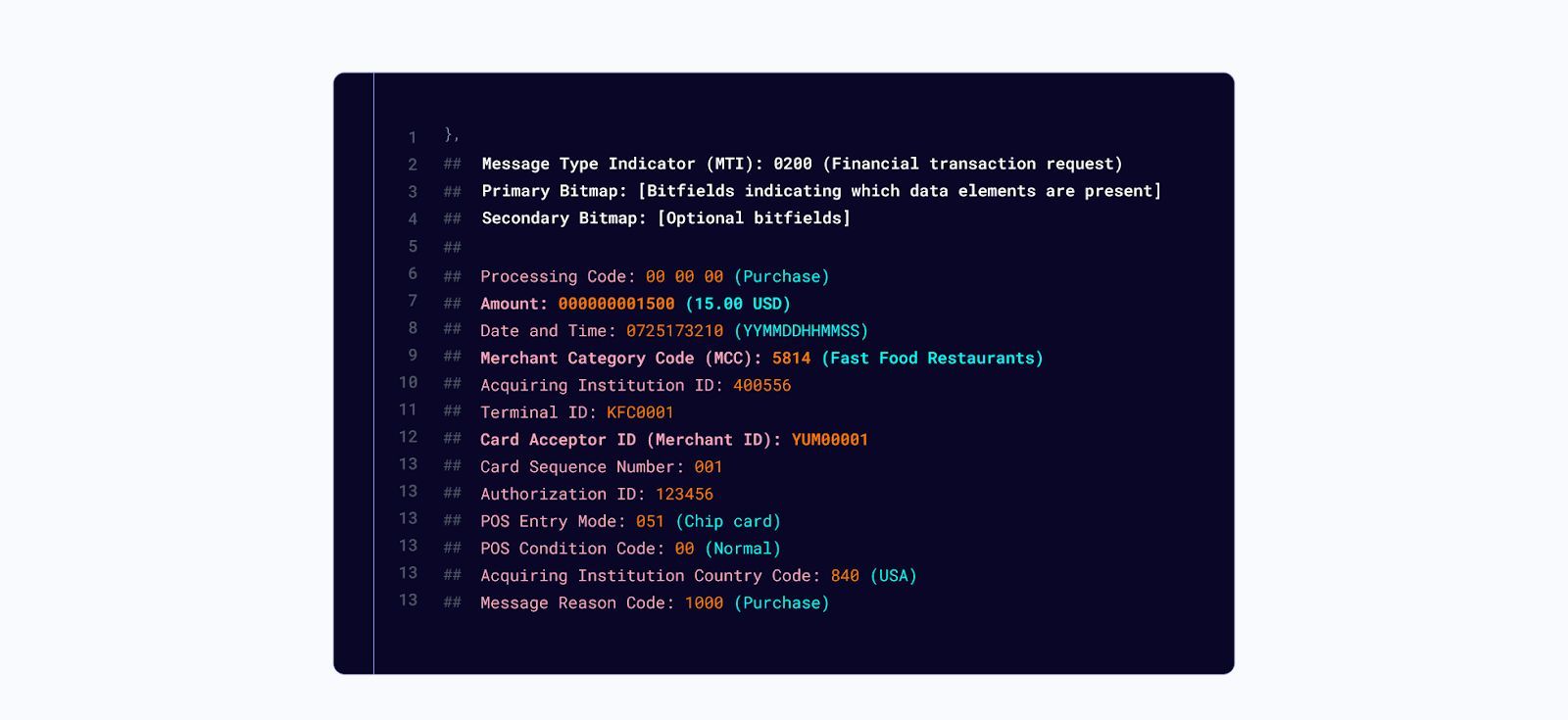

In this simplified transaction, a user has bought $15 worth of fast food at Yum. Yum! Brands is the parent company of KFC, Taco Bell, and Pizza Hut. So the first question is, which brand did they spend at?

Also, there are over 53,000 Yum Brands locations. Even Manhattan has 26 Taco Bells. How do we know if a user completed that purchase at that location? How do we know if it was a high fraud area? How do we know which brand it was?

If the fraud system relies on a Merchant Category Code, it could lead to either high fraud rates or false declines. Both are bad for business and bad for customers.

Here’s what it looks like with Spade’s merchant intelligence combined with Sardine’s device data and brain.

- Collect the true location of the user's mobile phone at the time of purchase. That is something Sardine provides today via our Device Intelligence capabilities.

- Identify the true merchant identity and link it to the transaction. That is provided today via Spade’s merchant intelligence capabilities – with a single ID for every location or instance of a merchant, no matter how the name shows up in the descriptor or which Merchant ID is present

- Collect the true merchant location and link it to the transaction. That is provided today via Spade’s merchant intelligence capabilities.

- At the point of transaction authorization, combine these data points to provide a real-time fraud assessment. Sardine’s rule engine, dashboard, and 🧠 pull together any data source, enrich it, and make real-time decisions.

20/20 vision for e-Commerce

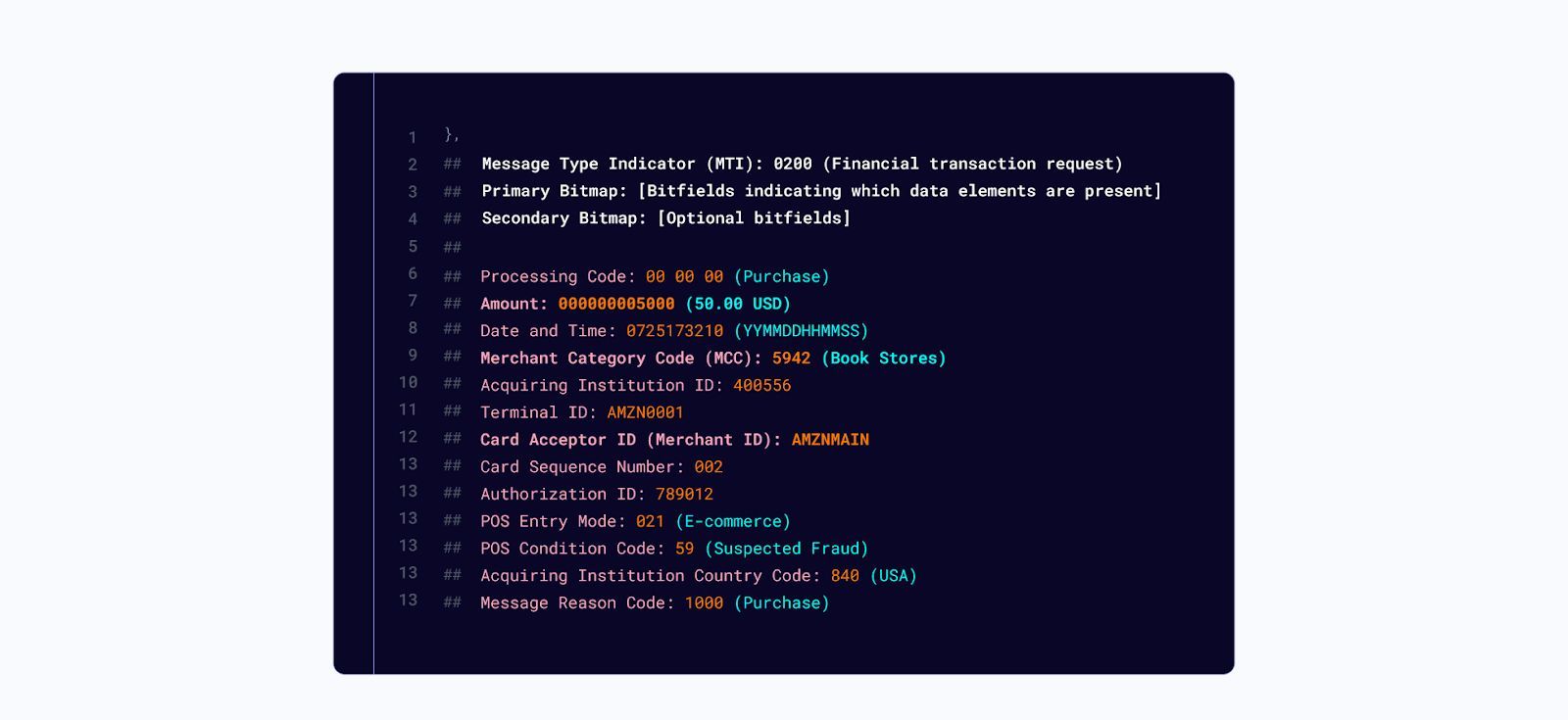

In this example, we see a user purchasing $50 on Amazon. But we don’t know if that's electronics, books, or digital content, each with its own fraud risk. The MCC Code is set to “book stores,” which doesn’t capture everything Amazon does. The transaction is suspected of fraud from the message, but how can we validate that? Might this lead to a false decline?

We can make this much higher resolution with Spade and Sardine

- Collect device history data. If this device has routinely behaved well with low fraud risk at multiple merchants, even if the card is new, we have higher confidence this is not a fraud.

- Collect user behavior signals. Is this new card purchase on this device typing, swiping, or tapping their keys in the same way they always do, or has something changed? If something has changed, this could be a fraud. If it’s the same, it likely isn’t.

- Sub-categorize the merchant. Was this an AWS transaction, an Amazon Prime subscription, or a Kindle purchase? The answer makes a meaningful difference to your decisioning.

- Build custom rules. Sardine allows users to create new rules using no-code or low-code quickly. Users can select from a vast array of features (which include data points submitted to the Sardine API, enrichments done by Sardine through consortium risk signals, and derived fields by Sardine’s proprietary models). Then, add outcome actions and submit the rule in Live or Shadow environments.

- Real-time risk scoring. At the point of transaction authorization, combine these data points to provide a real-time fraud assessment. Then, approve, deny, or flag a transaction for review.

Get a real-time view of the true merchant ID, pull in any data you like, build a custom rule, and decide whether to approve the transaction auth.

Less false positives. More conversion. Less fraud.

Lovely.

Combining better vision 👀 with better sense-making 🧠

The fraud squad needs better vision and better sense-making.

Imagine you're hiking without your glasses, trying to make your way down a mountain. Data enrichment is like putting on glasses -- letting you see the right path to take and even giving you enough clarity to avoid walking into the bear in front of you that you thought was a tree.

It’s no different in fraud detection.

With better vision provided by Spade and other data signals, the fraud squad gets a complete picture of the transaction. Sardine’s dashboard, rules engine and machine learning features operate in real-time. This means merchant intelligence, device, behavior, and any other signal (including bank consortia, email, telco, and many others) can be used during the authorization of a transaction.

When your senses and your brain are in real-time, your transaction approvals and declines are, too.

Approve good transactions.

Catch more fraud with Sardine and Spade.