Credit Underwriting

Credit Underwriting

Real-time credit risk decisioning for safer growth

Automate underwriting and assess consumer and business credit risk using bureau, cash-flow, identity, and behavioral signals.

Approve more qualified applicants

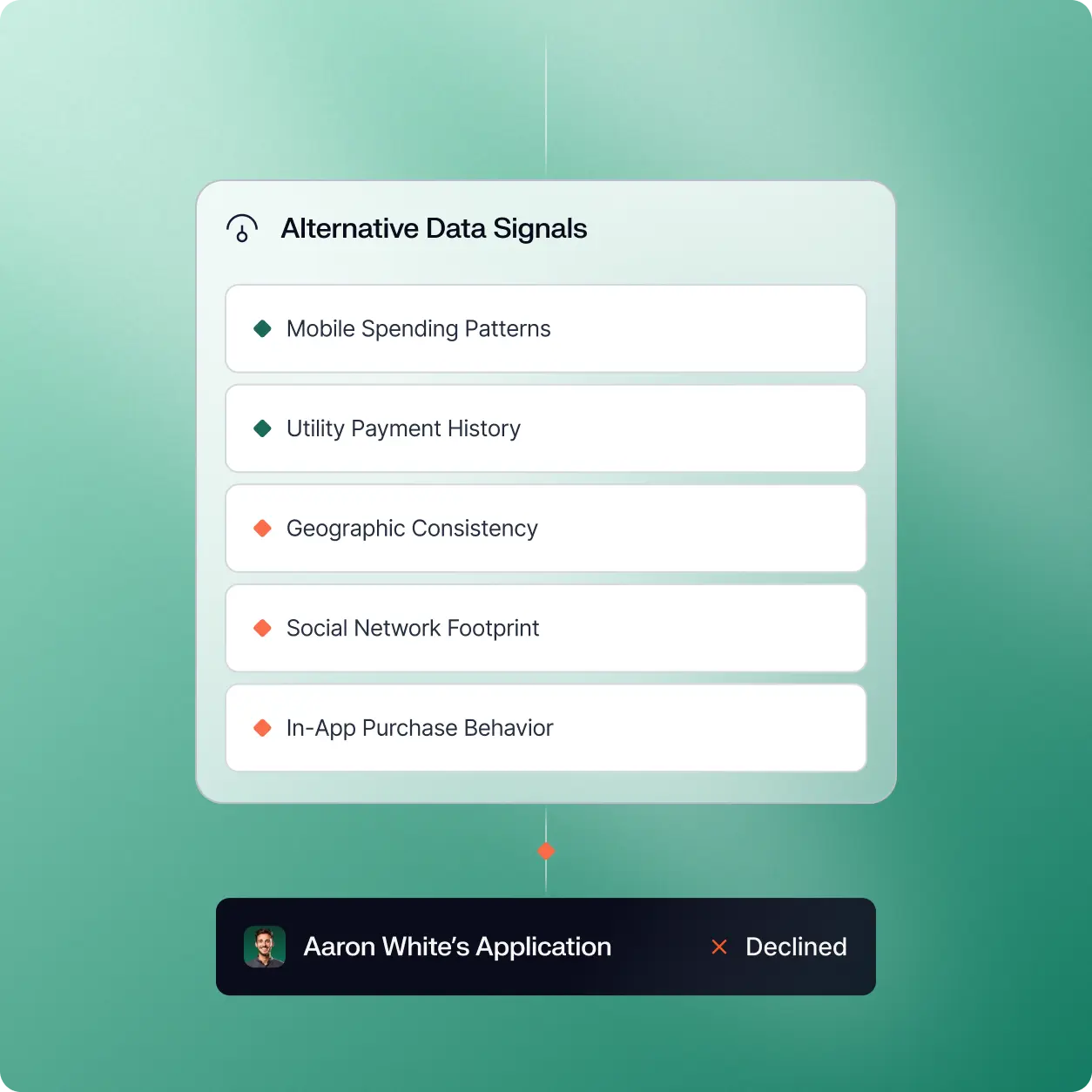

Combine traditional bureau data with alternative data and proprietary identity signals for better approvals.

Automate underwriting workflows

Replace manual reviews with configurable workflows that apply credit policies consistently.

Reduce default and audit risk

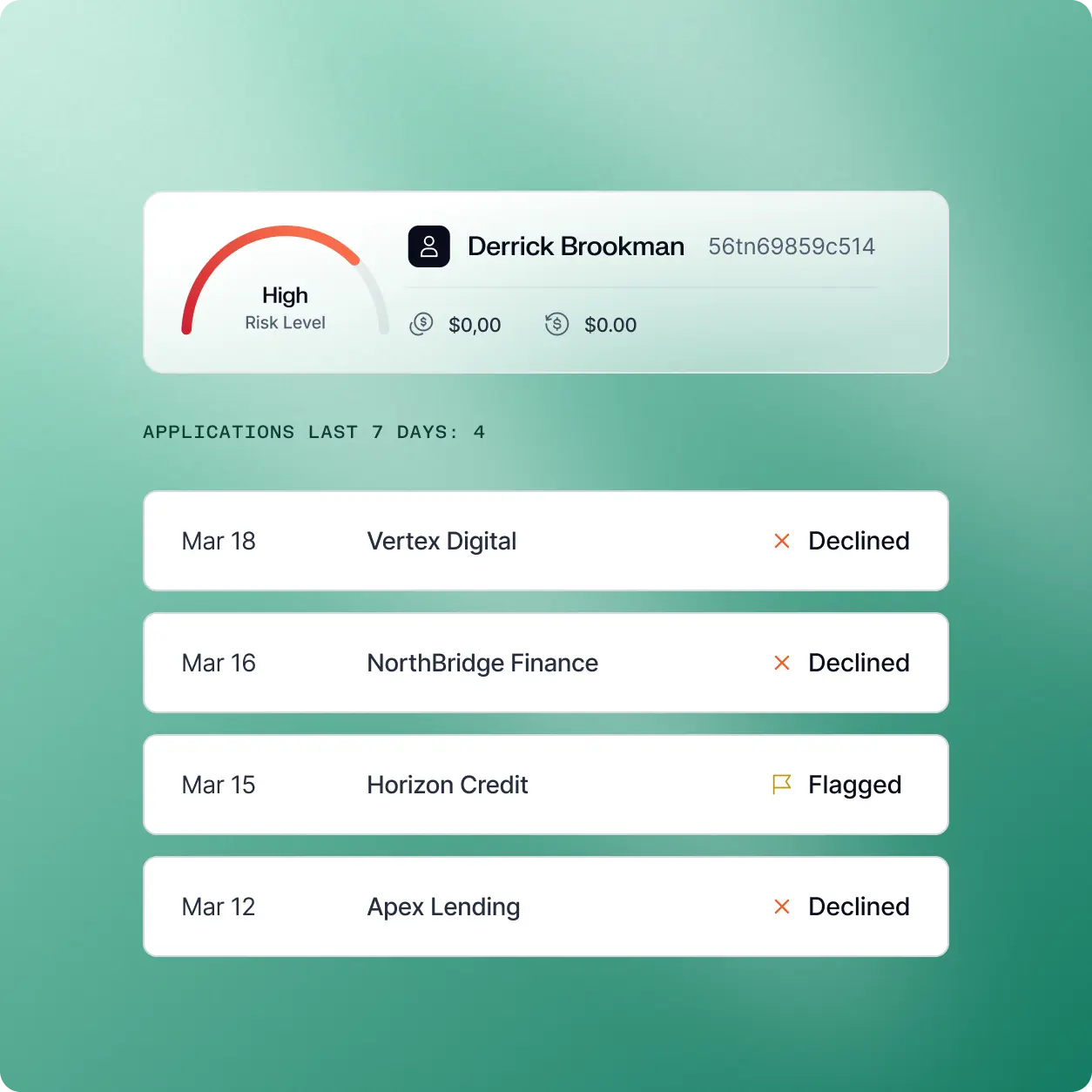

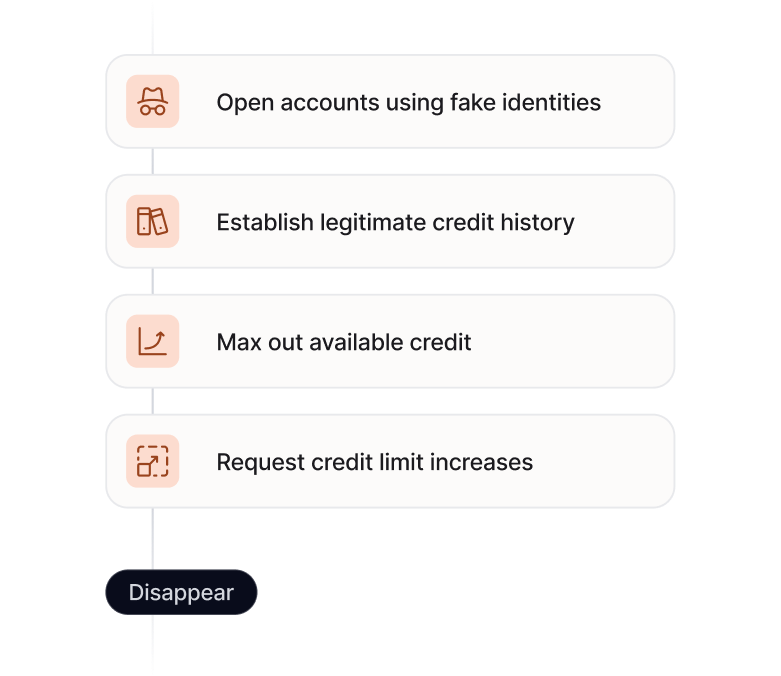

Detect bust-out fraud, first-party risk, and early warning signals before exposure grows.

Assess true repayment capacity and detect risk before exposure grows.

Consumer Credit

Consumer credit decisioning

Assess individual applicants using unified bureau, cash-flow, identity, and behavioral signals in one real-time workflow.

Business Credit

Business credit decisioning

Assess business borrowers using unified credit, ownership, transaction, and behavioral signals in one decisioning engine.

Seller Financing

Marketplace and platform financing

Underwrite individual and business sellers using proprietary platform data alongside traditional credit signals.

Incorporate order history, fulfillment metrics, revenue trends, dispute rates, and platform tenure directly into underwriting decisions.

Use configurable decisioning workflows to blend platform data with bureau, identity, cash-flow, and fraud signals.

Identify fake transactions, circular trading, related accounts, and inflated volume used to qualify for financing.

Automate AI-assisted credit risk decisions

Research applicants, surface hidden risk, and continuously optimize underwriting outcomes with structured oversight.

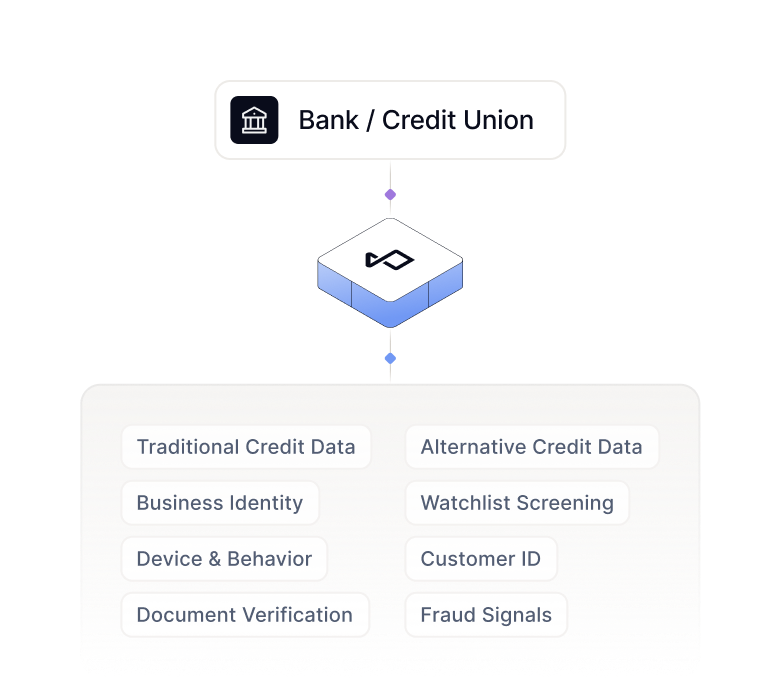

Backed by a unified credit and risk intelligence platform

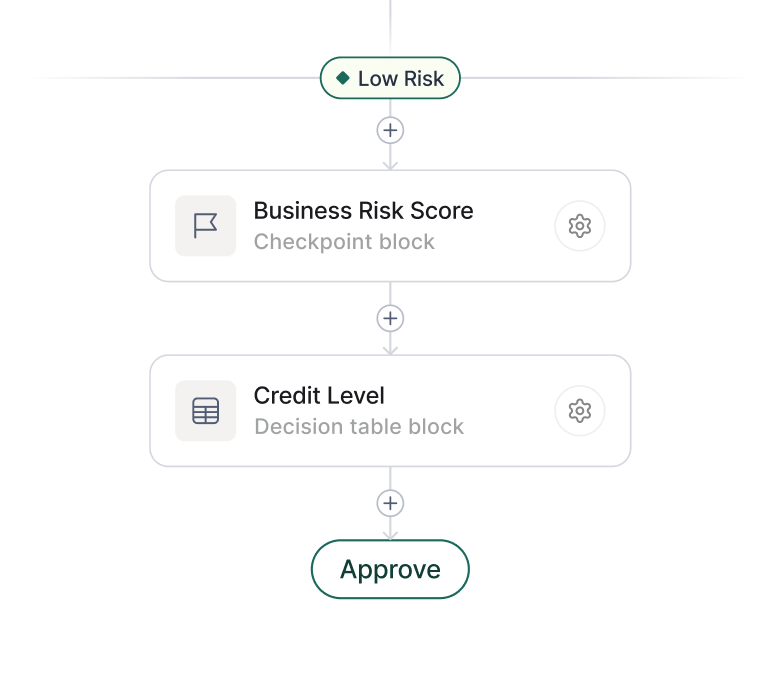

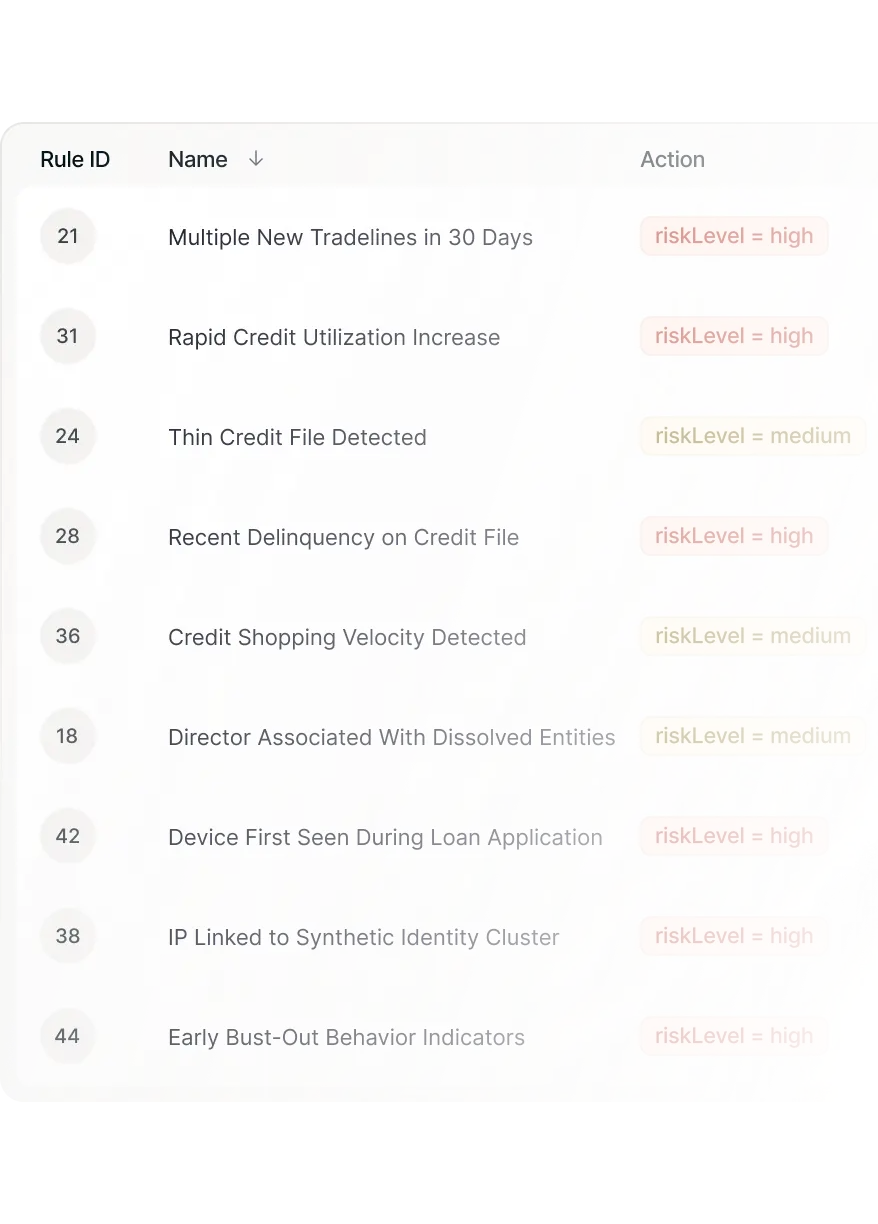

Rules & Workflows

Design credit workflows without engineering support

Define how applications move through approval, decline, review, and limit-setting using configurable workflows.

Machine Learning

Detect early signs of credit risk

Combine proprietary device & behavior signals with ML to identify early signs of default risk, bust-out behavior, and repayment instability.

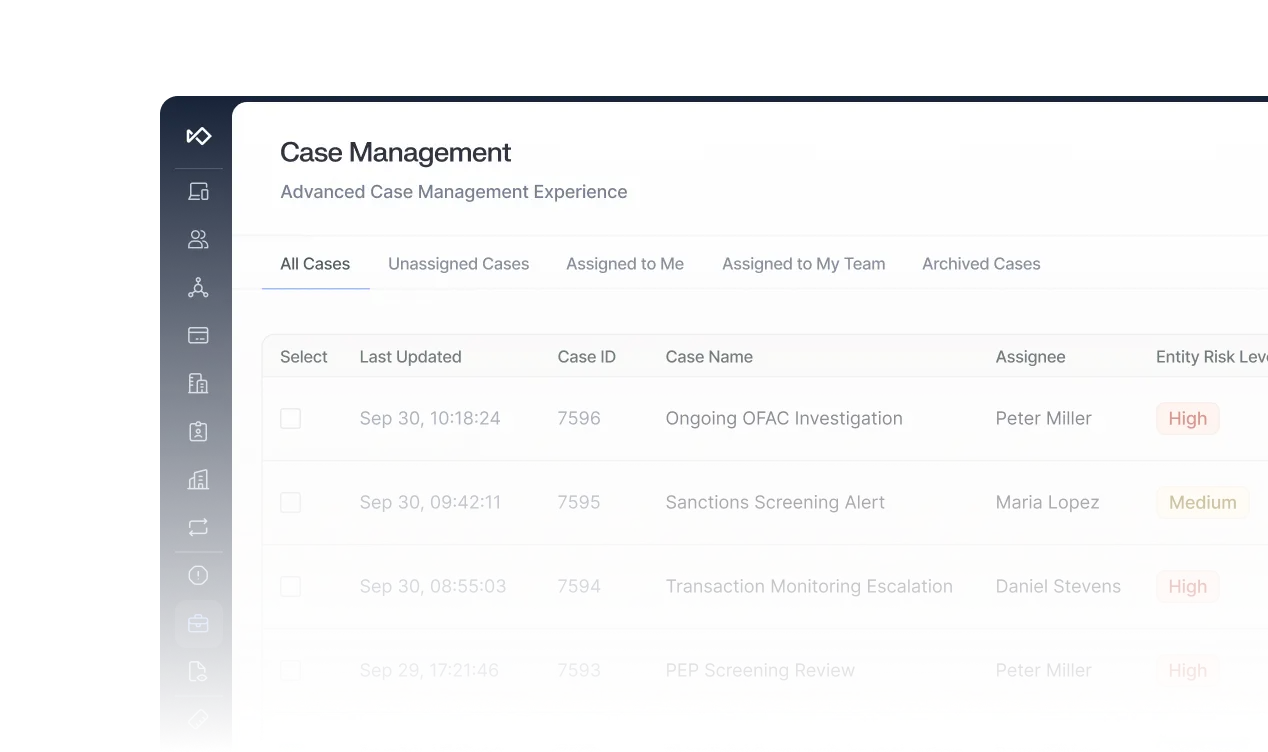

Case Management

Review and decide with full context

See application data, model outputs, and policy decisions in one place to move faster and make better underwriting decisions.

Increase approval rates without additional risk

Frequently asked questions

How does Sardine combine credit and fraud signals in a single underwriting decision?

Sardine evaluates bureau data, cash-flow signals, identity verification results, device intelligence, and fraud indicators within one unified workflow engine. Rather than running separate credit and fraud systems that produce disconnected scores, all signals feed the same rules engine and machine learning models. This allows risk teams to adjust thresholds based on combined context, detect loan stacking or synthetic identity patterns early, and apply differentiated approval, limit, or review logic in real time. Every decision is fully explainable and logged with structured audit trails to support governance and regulatory review.

How can we experiment with new underwriting strategies without engineering delays?

Sardine’s Workflow Builder and Rule Suggestion Agent allow risk teams to build, test, and deploy strategies directly without relying on engineering resources. Teams can create rules in natural language, search across 12,000+ available features, run backtests or shadow deployments, and deploy updates with one click. The anomaly engine continuously monitors traffic and suggests new rules when unusual behavior patterns emerge, enabling operators to iterate quickly while maintaining full auditability and structured oversight.

How does the OSINT Agent support underwriting?

The OSINT Agent automates open-source research during underwriting and enhanced due diligence by searching news outlets, social media, corporate registries, and public databases automatically. It extracts relevant findings into structured summaries with clear risk insights, helping teams uncover adverse public signals that may not appear in bureau data alone. By reducing manual research time by up to 90%, the agent enables faster decisions while ensuring public risk indicators are incorporated before exposure grows.

How does Sardine ensure underwriting decisions remain explainable and audit-ready?

Sardine centralizes credit data, fraud signals, reviewer actions, and decision logic in a single system of record. For every underwriting decision, the platform logs rule triggers, model outputs, overrides, and supporting evidence, generating clear reason codes and regulator-ready summaries. Through the Agentic Oversight Framework, AI-driven decisions can operate in copilot or autonomous mode with ongoing human calibration, ensuring governance, transparency, and defensibility without sacrificing automation.

How does Sardine detect bust-out and first-party fraud before losses occur?

Sardine correlates bureau data, transaction behavior, device intelligence, identity signals, and behavioral anomalies to surface early indicators of elevated default or misuse risk. By analyzing patterns such as abnormal usage shifts, infrastructure reuse across applications, and identity inconsistencies, the system helps detect bust-out and first-party fraud before capital is extended. The anomaly engine further strengthens detection by continuously monitoring traffic and suggesting new rules when emerging patterns appear, allowing teams to respond before exposure compounds.