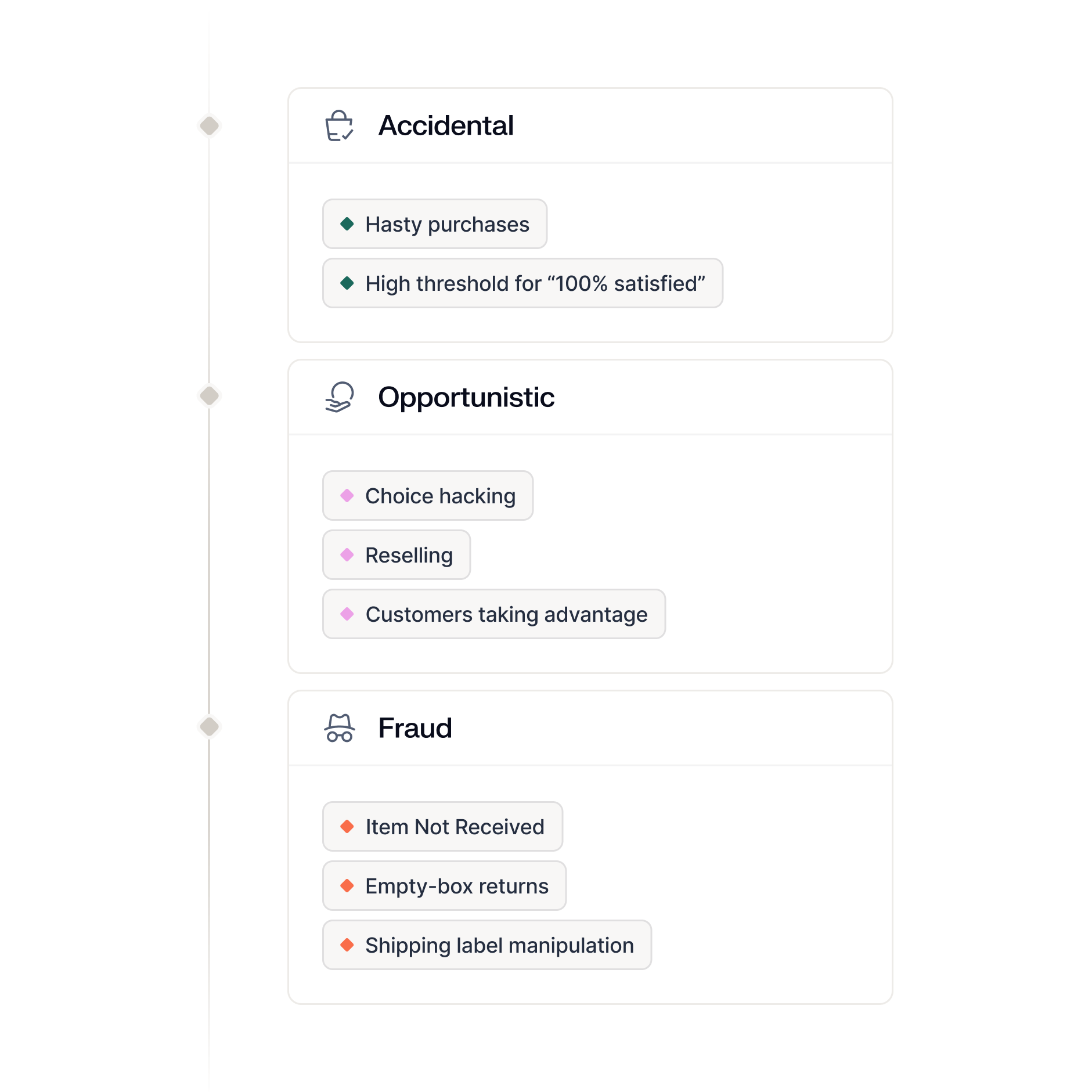

First-Party Fraud

First-Party Fraud

Stop policy abuse without impacting legitimate customers

Detect early signs of promo abuse, refund fraud, and chargeback fraud before they turn into losses.

Strong abuse protection for merchants, marketplaces, and platforms

Stop hidden revenue leaks

Use cross-industry consortium insights to uncover fraudsters and patterns that would be invisible in your own data alone.

Shield your best customers

Keep the experience smooth for your users with targeted controls that stop abuse without broad restrictions.

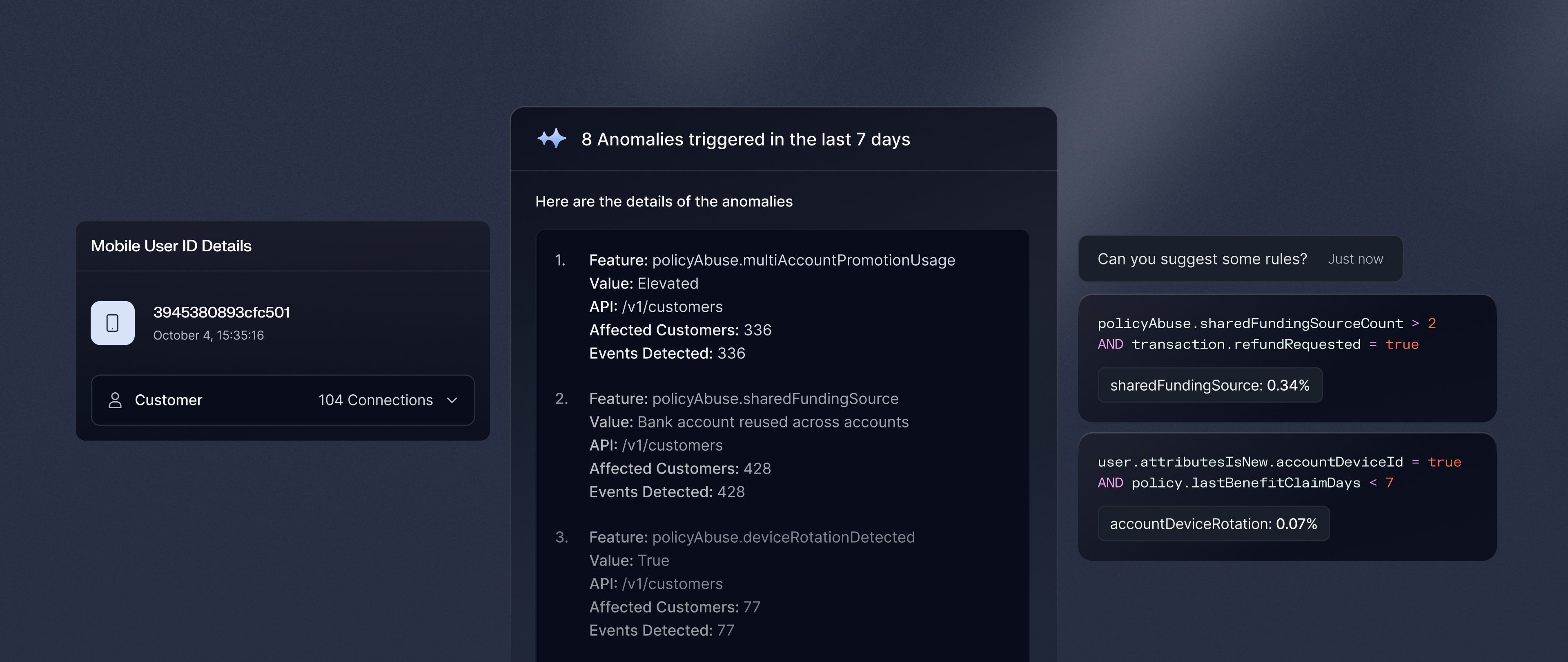

AI that adapts defenses

Agents analyze your traffic and proactively recommend rules to prevent fraud attacks and abuse patterns

Leverage device, behavior, and consortium signals to stop abuse earlier

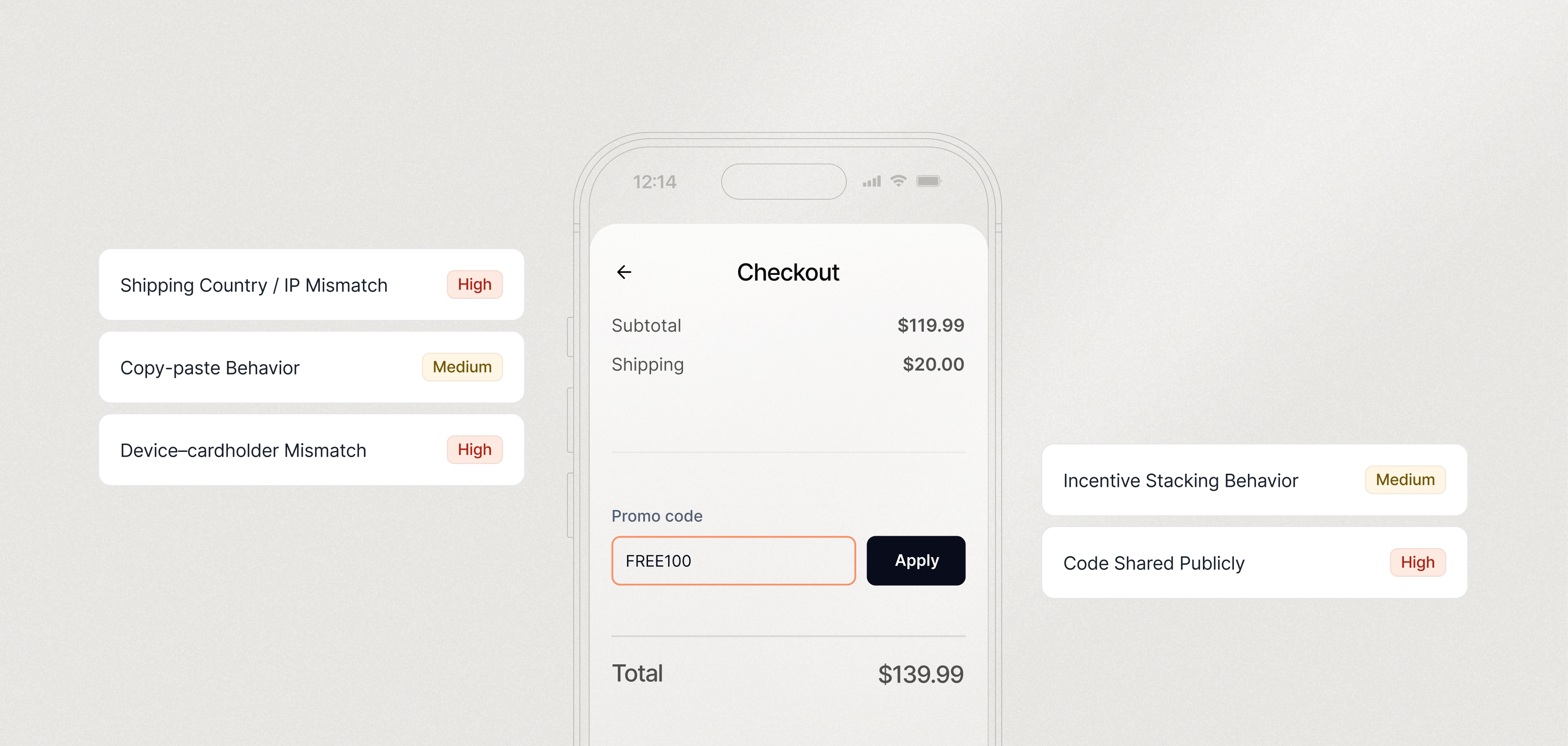

Promo Abuse

Prevent promo abuse

Reduce promo farming, code sharing, and incentive stacking without adding friction for legitimate customers.

Surface accounts sharing the same device fingerprints, phones, names, or emails to create accounts.

Identify referral rings and organized farming by correlating activity across accounts, sessions, and the broader network.

Apply controls at the user, account cluster, or network level so you can stop abuse without broad promo restrictions.

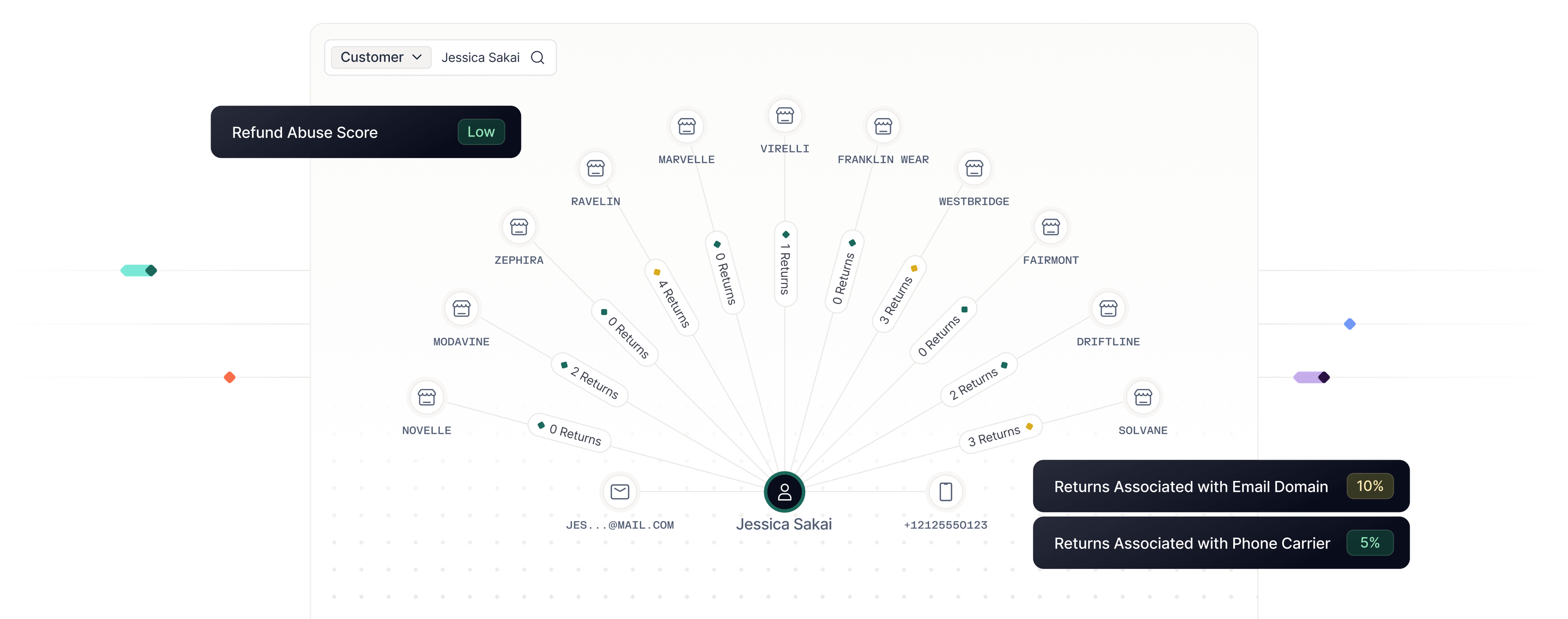

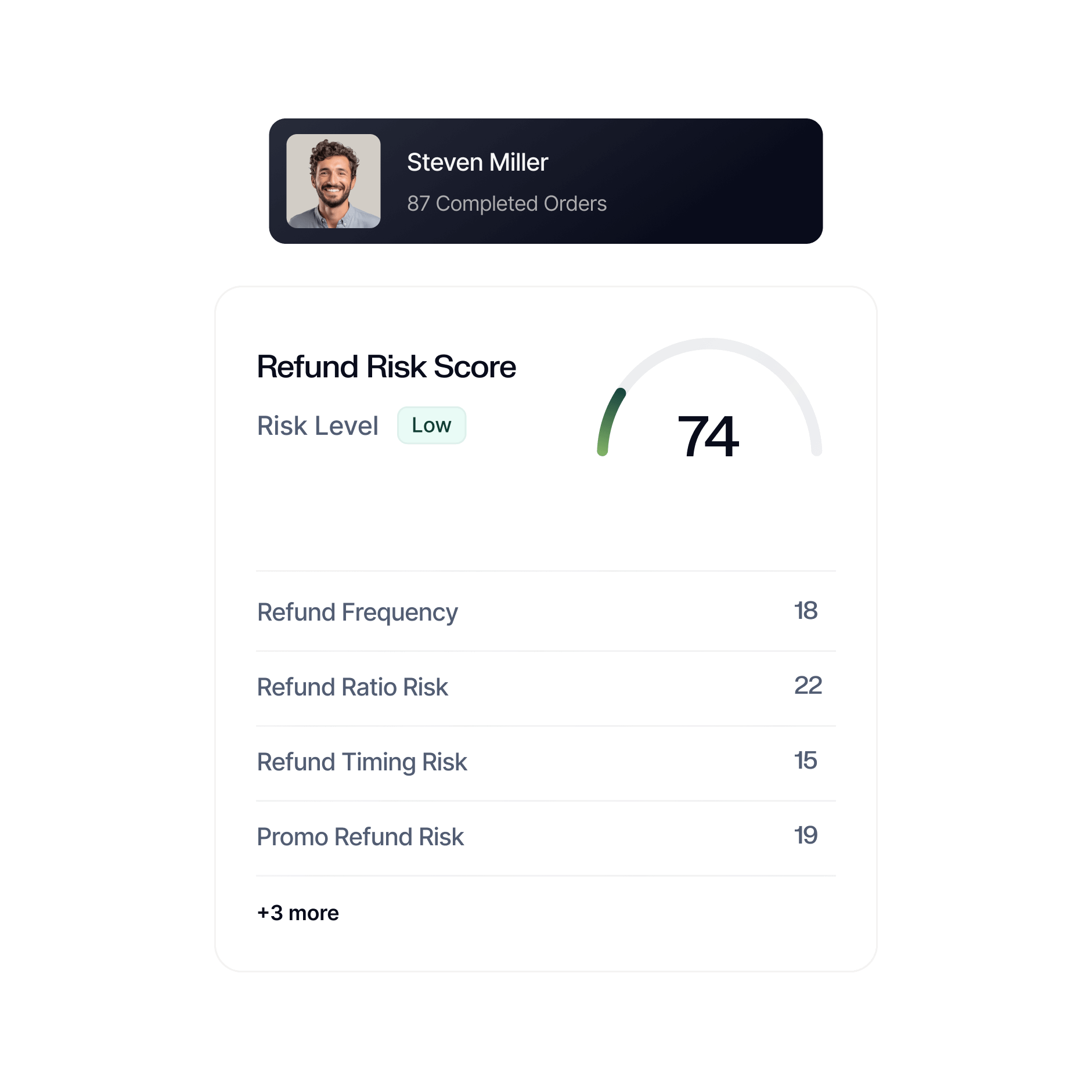

Refund Abuse

Protect margins while keeping policies flexible

Prevent users from exploiting your refund and return policies, from empty-box returns to fake delivery claims.

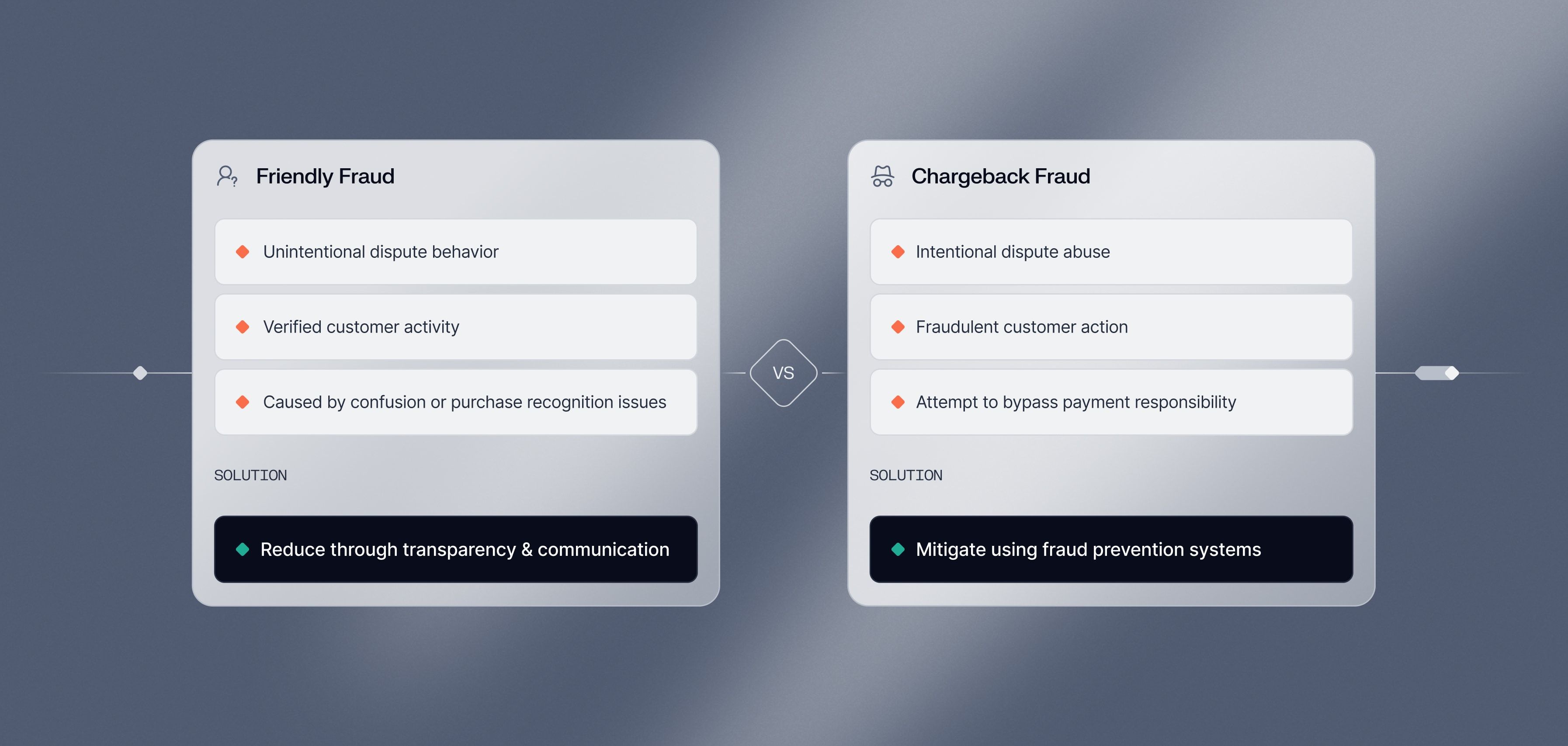

Friendly Fraud

Distinguish first-party abuse from legitimate chargebacks

Identify when cardholders falsely claim fraud on legitimate transactions to recover funds.

Use account access, device continuity, and payment history to confirm whether the cardholder was involved in the purchase.

Detect when checkout, fulfillment, and post-purchase behavior do not line up with a legitimate dispute.

AI agents help you build stronger disputes cases with evidence aligned to Compelling Evidence 3.0 and other issuer requirements.

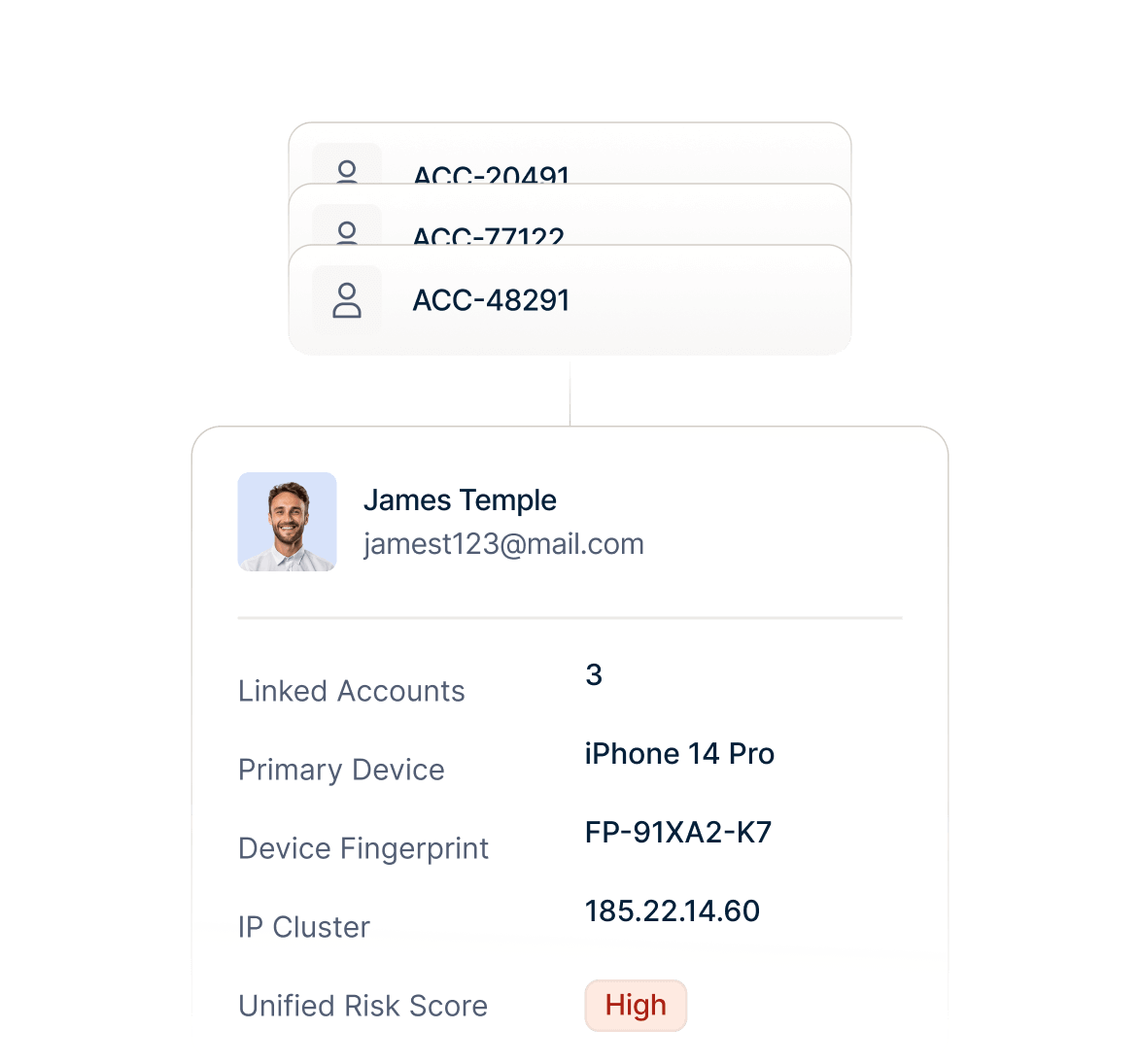

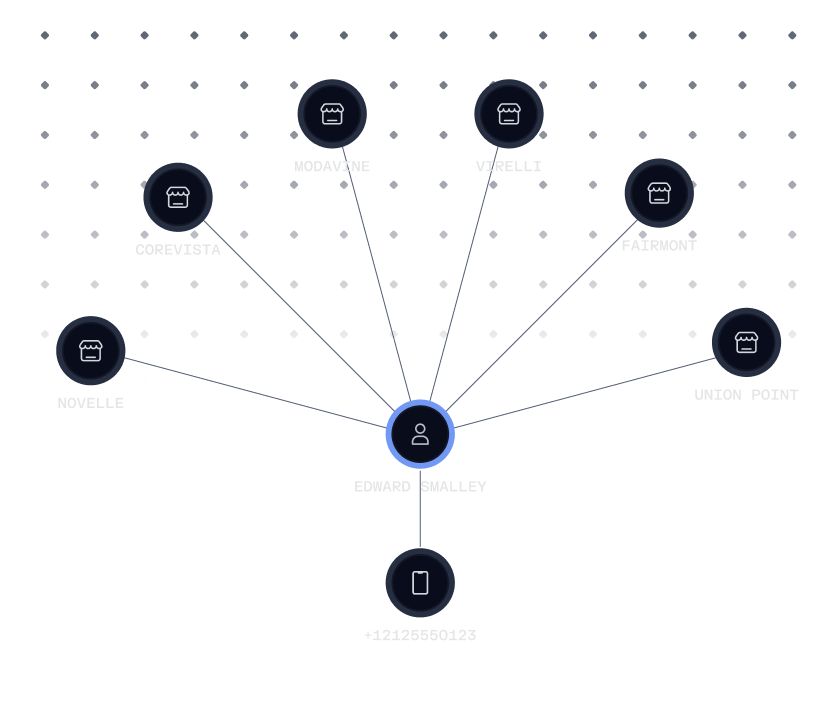

Multi-Accounting

Move from reacting to preventing abuse

Identify linked identities early so repeat abusers cannot re-enter your platform through new accounts.

AI agents that stop abuse faster, and more accurately

Investigate behavior, resolve routine abuse cases, gather evidence, and explain enforcement decisions in real-time.

Backed by the industry’s leading agentic risk platform

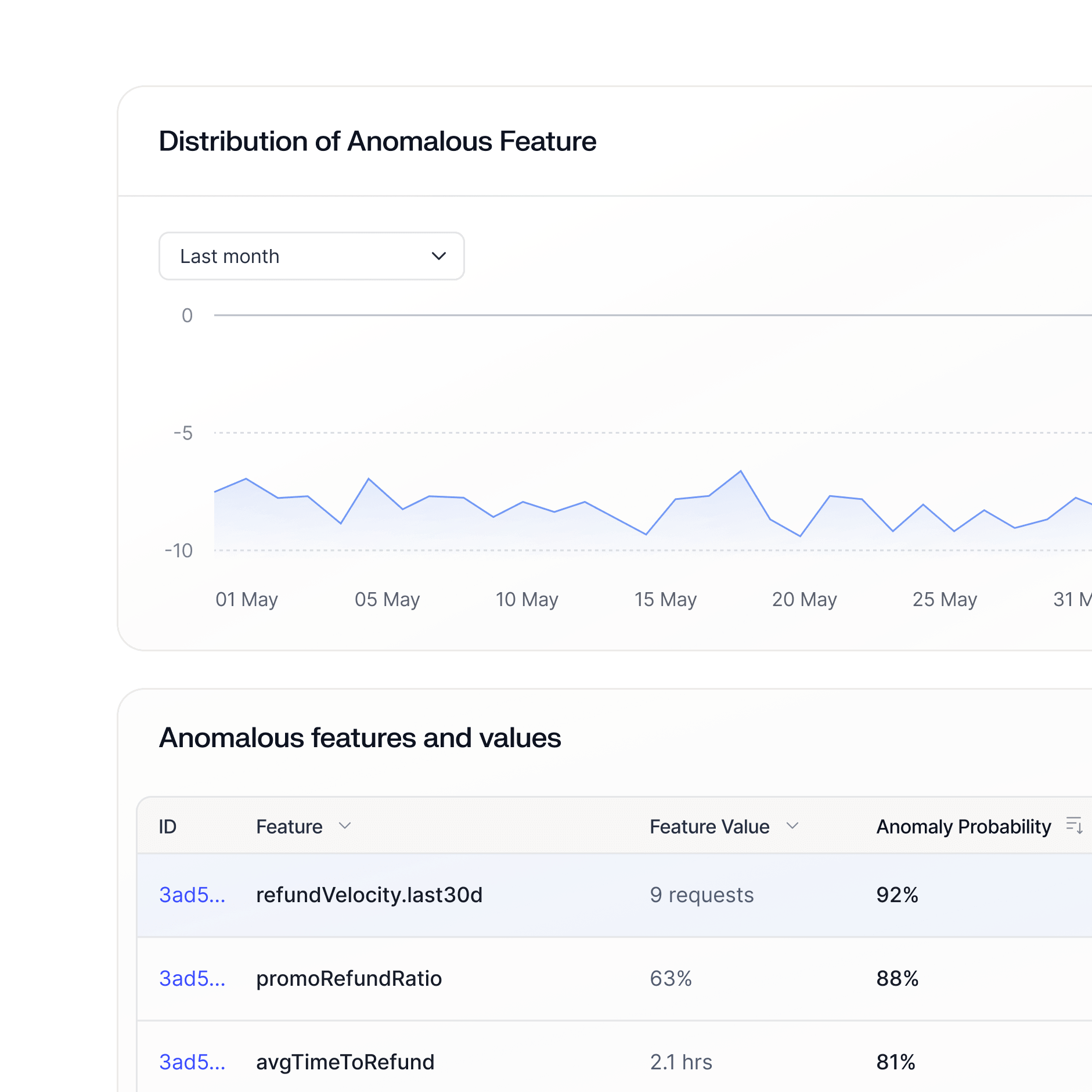

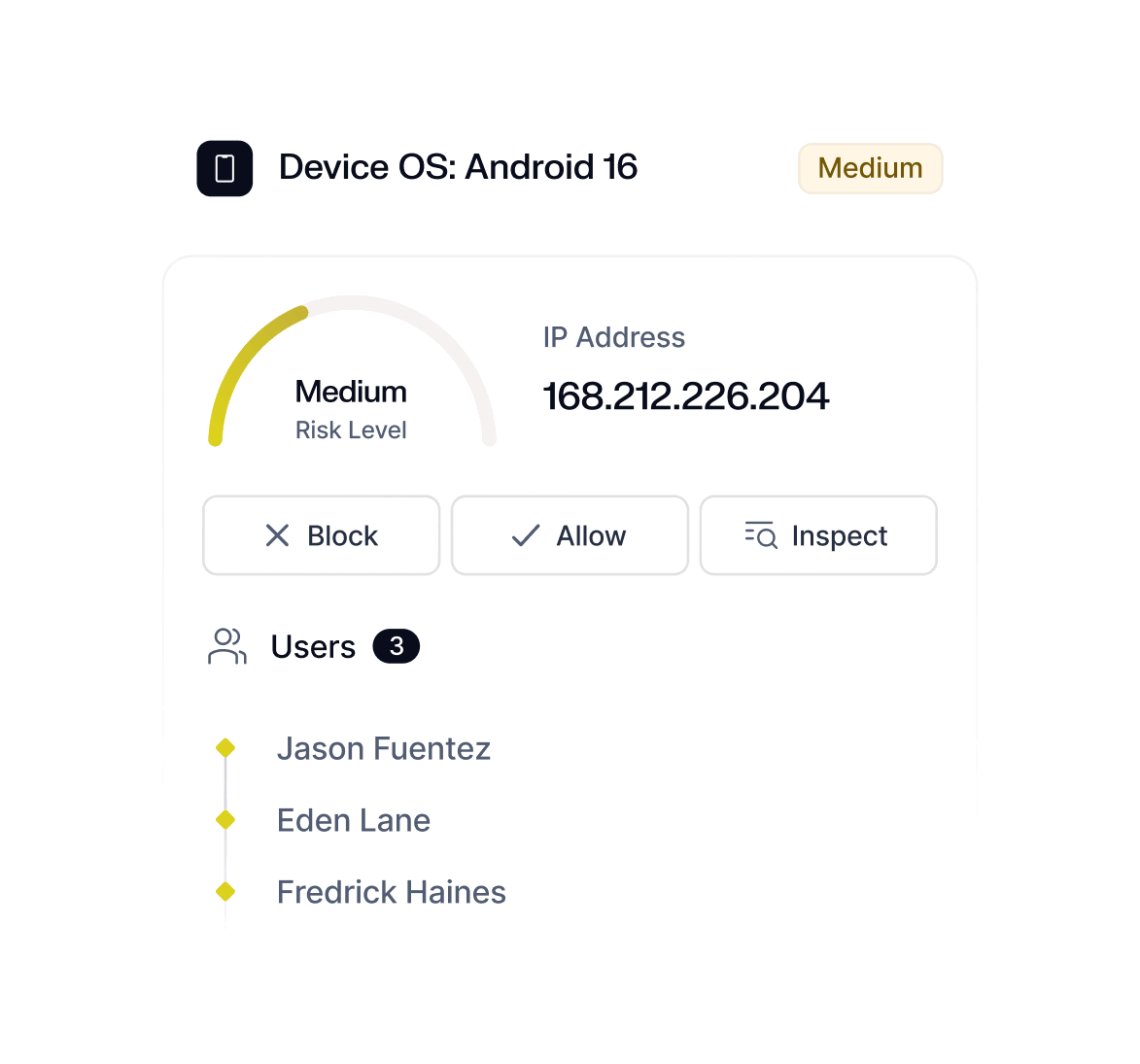

Device & Behavior

Predict abuse earlier

Device and behavioral biometrics distinguish loyal usage from repeat abuse, collusion, and scripted activity that appears legitimate alone.

Data Consortium

Expose repeat abusers

Leverage shared risk intelligence rooted in financial and behavioral activity.

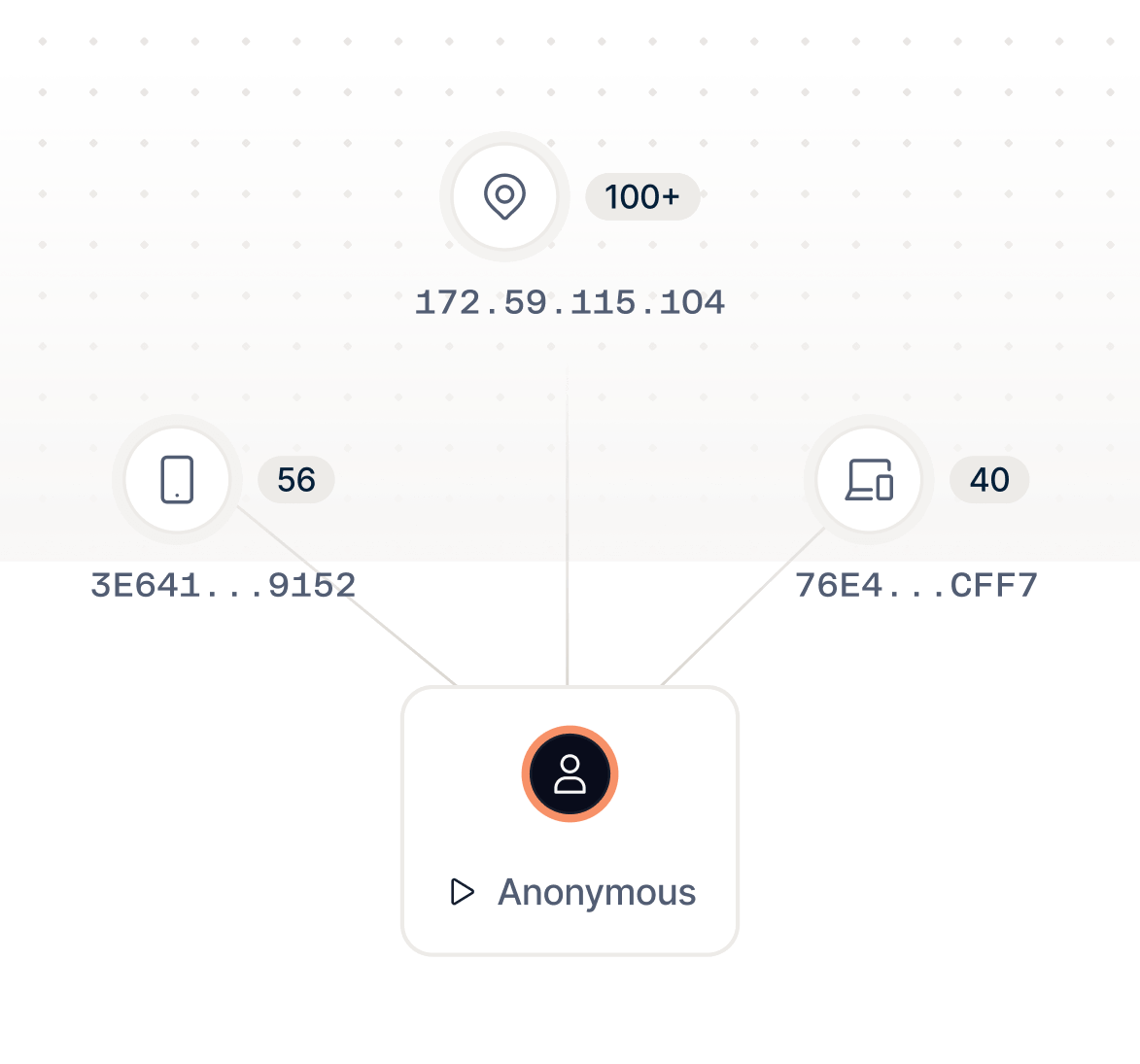

Fraud Investigations

Unravel abuse networks

Reveal coordinated abuse by linking customers across accounts, devices, and payments.

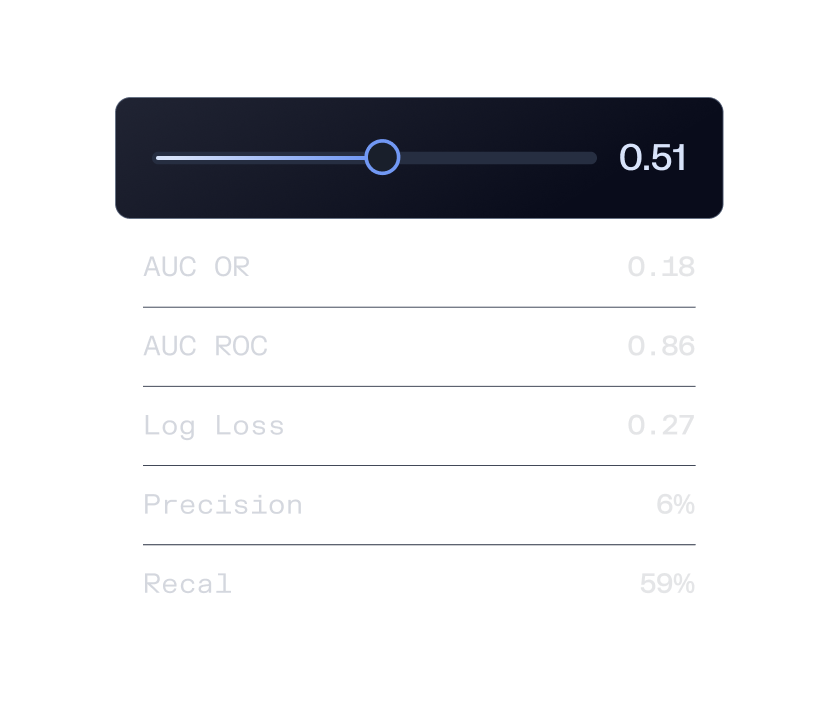

Machine Learning

Improve accuracy over time

Use outcome-based models to surface early abuse signals and reduce false positives.

Stop policy abuse without impacting legitimate customers

Frequently asked questions

How early can Sardine detect policy abuse and first-party fraud?

Sardine evaluates customer behavior during browsing, checkout, login, and refund initiation, not just after transactions settle. By scoring device intelligence, behavioral biometrics, and network-level abuse signals in real time, risk can be identified before promos are redeemed, refunds are issued, or disputes are filed.

What data does Sardine use beyond commerce events?

Beyond order and refund data, Sardine analyzes device fingerprints, behavioral biometrics, identity reuse, payment history, consortium intelligence, and cross-merchant abuse signals. This broader visibility enables detection of repeat offenders and hidden abuse patterns that transaction data alone cannot reveal.

How does Sardine distinguish abusive behavior from loyal customer behavior?

Customers are evaluated longitudinally rather than per event. By combining historical usage patterns, device consistency, refund and promo velocity, and ecosystem context, Sardine preserves low-friction experiences for trusted users while escalating controls only when abuse risk materially increases. This reduces false positives while stopping serial refunders and promo farmers early.

How does Sardine detect coordinated abuse and multi-accounting rings?

Entity resolution and graph analysis link accounts across devices, sessions, payment instruments, and behavioral attributes. This exposes multi-accounting, referral abuse, and coordinated fraud rings even when users rotate emails, phones, or credentials.

Can policy abuse be stopped before refunds, credits, or replacements are issued?

Yes. Abuse risk is evaluated at the moment value is requested. Controls such as step-ups, delays, limits, or denials can be applied before refunds, credits, or replacements are approved, preventing losses rather than reacting after chargebacks occur.

How does Sardine adapt as abuse tactics change over time?

Machine learning models and AI agents continuously learn from outcomes across refunds, promos, disputes, and chargebacks. Abuse risk signals recalibrate automatically as behavior shifts, reducing reliance on static rules or reactive policy tightening.

Can policy abuse controls vary by customer, product, risk tier, or channel?

Yes. Enforcement logic can be configured by customer tenure, lifetime value, product category, geography, order value, or acquisition channel. This enables risk-based controls where abuse concentrates while preserving customer experience for high-value segments.

How does Sardine reduce friendly fraud and chargeback losses?

By correlating delivery confirmation, login history, device consistency, and purchase behavior, Sardine separates legitimate disputes from first-party chargeback abuse. Automated evidence collection supports stronger representment and improved win rates.

How does Sardine prevent hidden revenue leaks from promo and refund abuse?

Serial refunders, promo stackers, and coordinated abuse rings are identified through behavioral anomalies, cross-account linking, and consortium intelligence. Early detection prevents margin erosion while maintaining flexible customer-friendly policies.