---

title: Stop Payment Fraud | Bank-Grade Fraud Detection Before Funds Move

source_page: https://www.sardine.ai/payment-fraud

canonical: https://www.sardine.ai/payment-fraud

format: text/markdown

description: Prevent ACH, RTP, FedNow, wires, and account-to-account fraud by analyzing transaction behavior, counterparties, and network risk before funds move...

---

**Quick links:** [Human page](https://www.sardine.ai/payment-fraud) · [Home](https://www.sardine.ai) · [Customers](https://www.sardine.ai/customers) · [Blog](https://www.sardine.ai/blog) · [Demo](https://www.sardine.ai/demo)

---

# Stop Payment Fraud | Bank-Grade Fraud Detection Before Funds Move

Prevent ACH, RTP, FedNow, wires, and account-to-account fraud by analyzing transaction behavior, counterparties, and network risk before funds move...

## Protect revenue across every payment rail

Approve more legitimate transactions while keeping your fraud rates low across cards, ACH, instant payments, and wallets.

## Smarter fraud controls for merchants

- 70%: Higher approval rate

- 98%: Decrease in manual reviews

### Approve more good payments

Increase authorization and SCA pass-through by routing low-risk payments through low-friction paths.

### Stop fraud before losses occur

Predict chargebacks, unauthorized payments, and returns before authorization or settlement.

### Lower fraud operations costs

Reduce manual workload and keep fraud costs predictable with automated reviews, disputes, and evidence collection.

## Accurate risk scoring across all payment methods

### Card Payments

Stop card fraud before authorization, not after disputes

- Analyze checkout behavior, device risk, and cardholder signals

- Approve more transactions with low-friction routing for low-risk payments

- Automate dispute evidence collection to improve chargeback win rates

### Bank Transactions

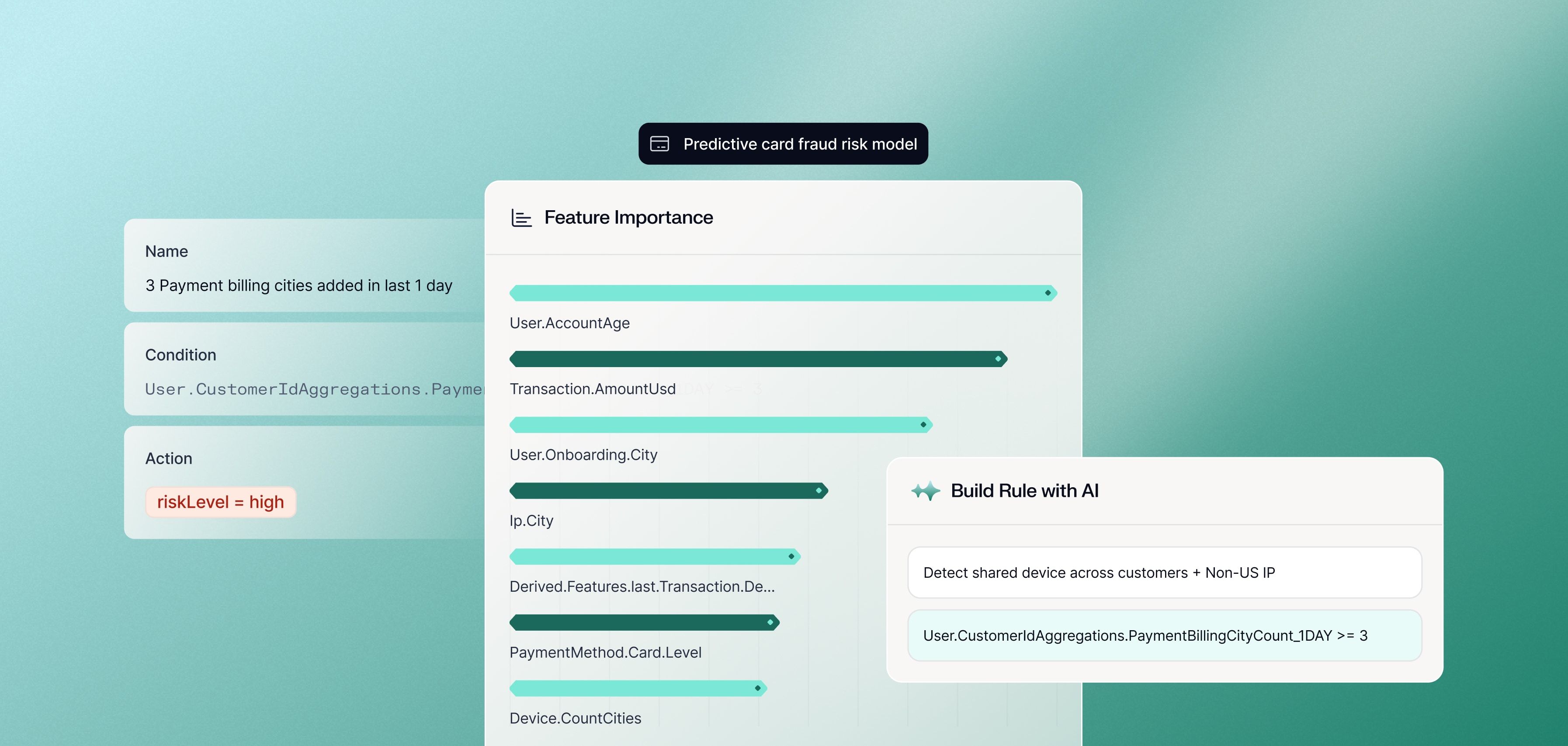

Reduce ACH returns and unauthorized debits before funds move

- Verify account ownership and ACH eligibility in real-time before initiating transfers

- Predict non-sufficient funds, unauthorized debit exposure, and known abuse signals

- Detect mule accounts and shared bank details using device and behavioral context

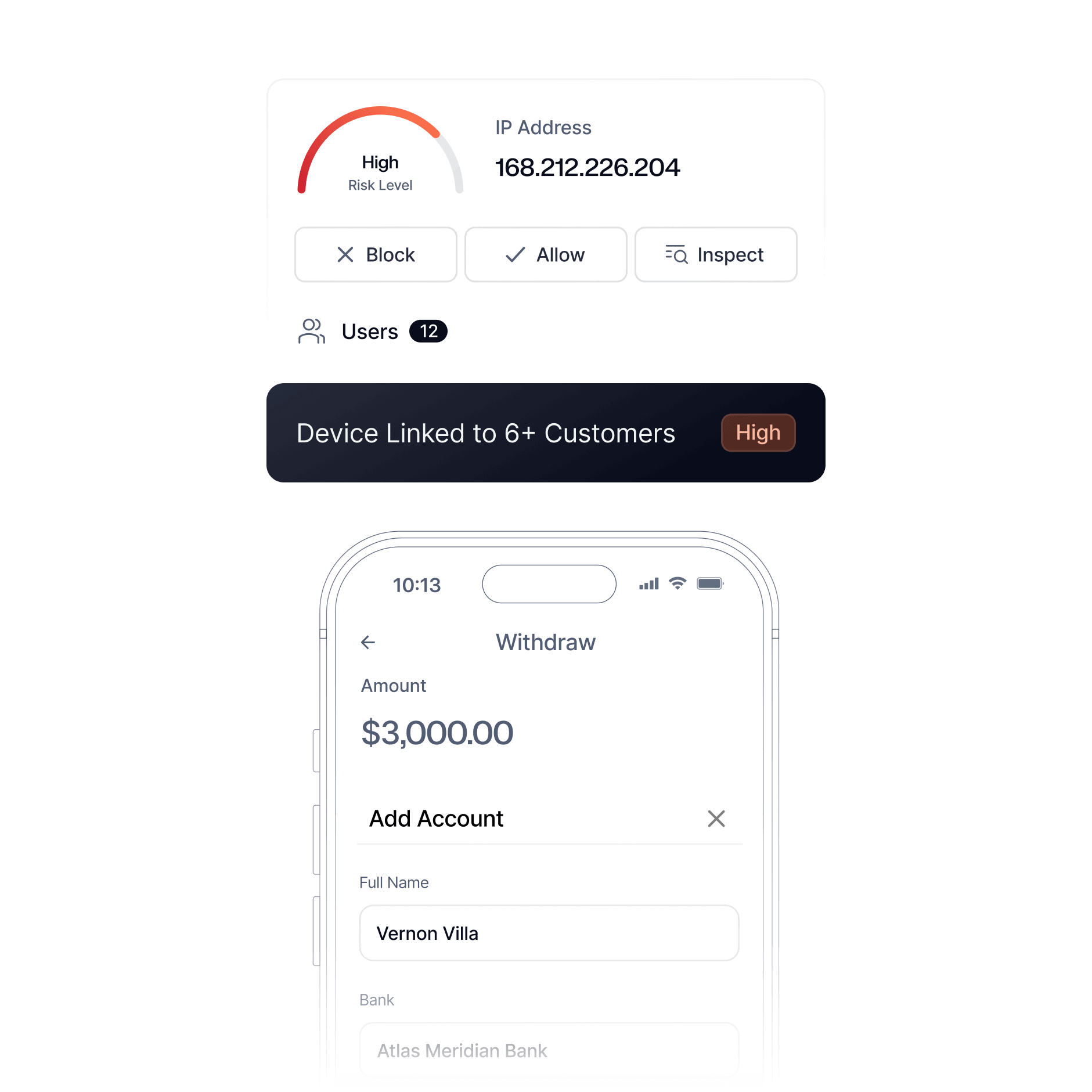

### Instant Payments

Protect RTP and FedNow rails without introducing latency

- Validate account ownership and session context within the instant payment window

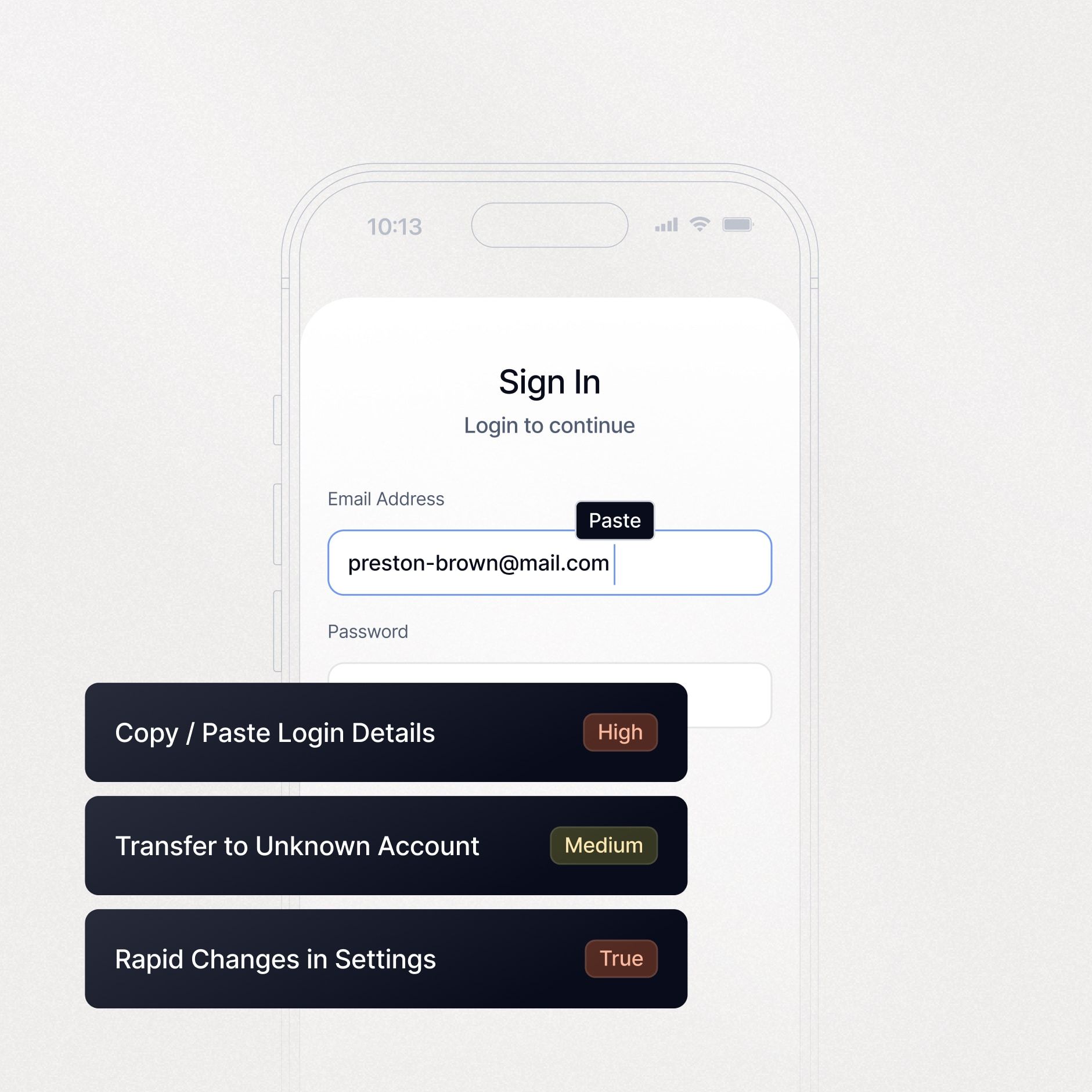

- Flag high-risk account changes and newly linked accounts before funds are released

- Stop account takeover-driven payments before irreversible transactions execute

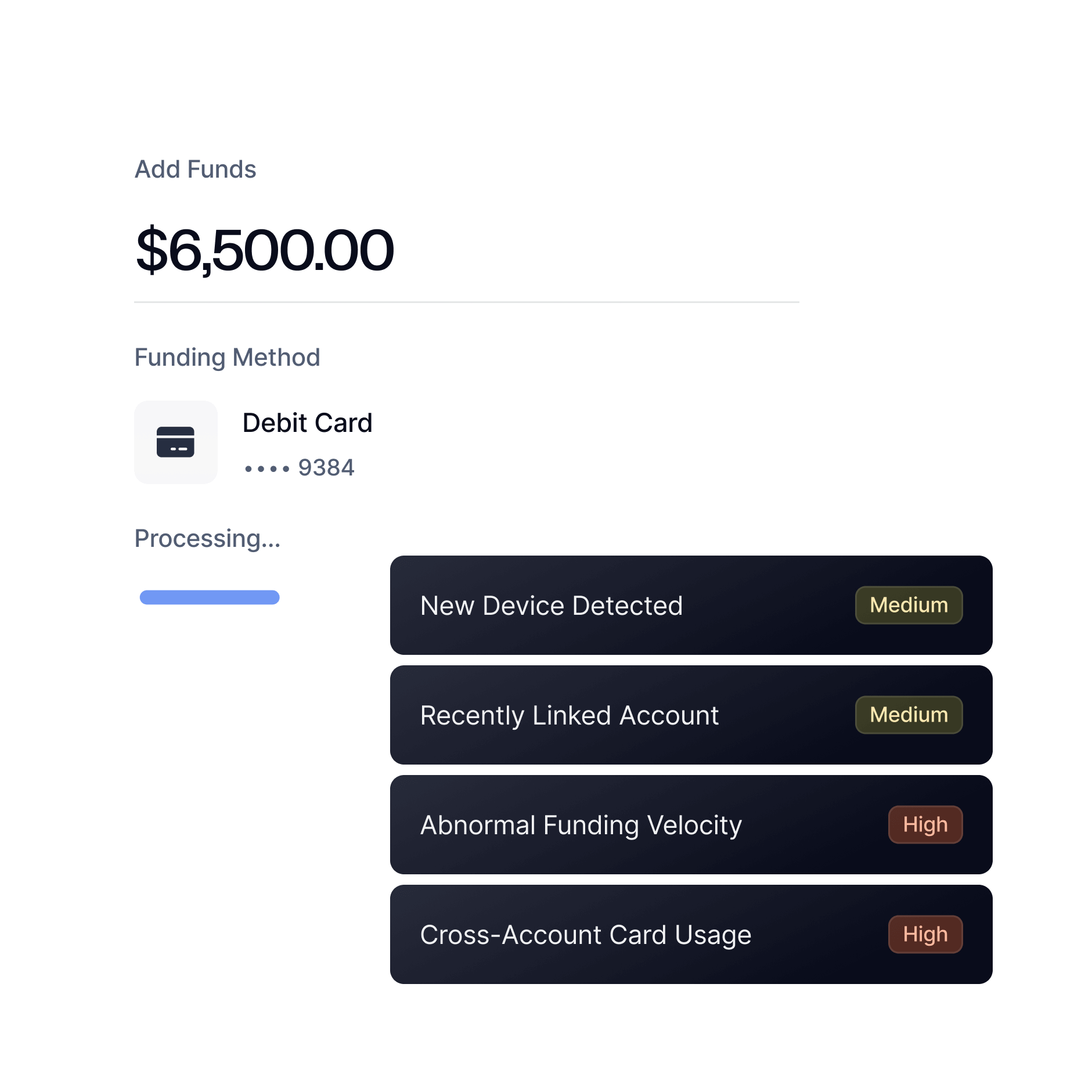

### Digital Wallets

Control deposit and cashout risk without disrupting legitimate users

- Block stolen card and bank credentials used to fund wallet accounts

- Detect rapid deposit-spend-withdraw cycles and mule-like movement between accounts

- Prevent ATO-driven funding changes, payment method cycling, and bonus exploitation

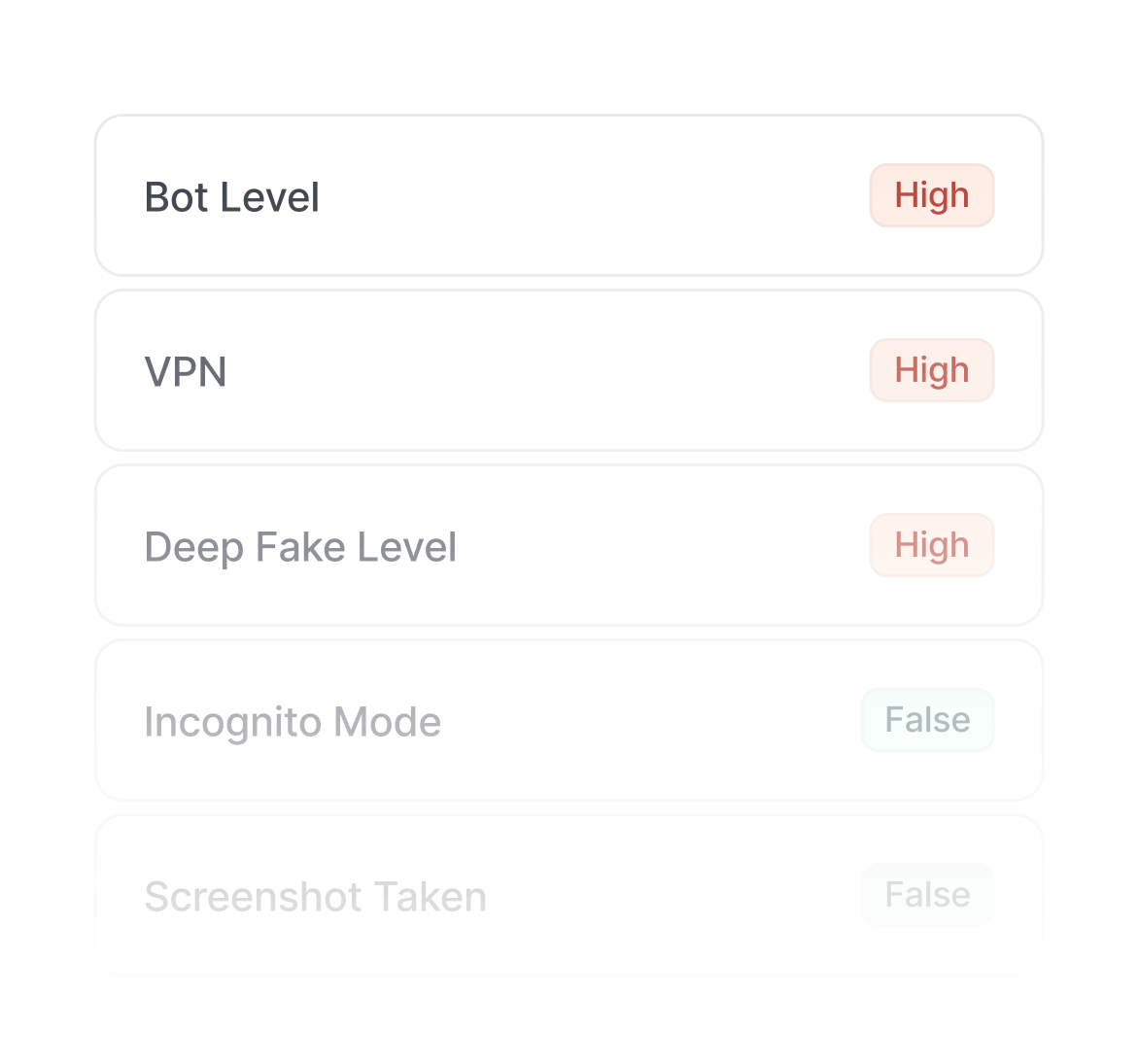

## Go beyond transaction-level data with device, behavior, and network intelligence

## Card-not-present transactions

Ecommerce Fraud

Stop card fraud so you can accept legitimate payments at checkout now and ship goods later.

### Generate pre-authorization risk scores

Analyze checkout behavior, device risk, shipping address signals, and cardholder verification to detect fraud earlier.

### Create, modify, and backtest rules

Build no-code workflows that approve, step up, decline, or route to a chargeback guarantee solution based on risk thresholds.

### Improve chargeback win rates

AI agent reviews disputes, pulls compelling evidence and submits it to the acquirer automatically.

## Marketplace payments

Marketplace Fraud

Facilitate payments between buyers and sellers without exposing your platform to coordinated abuse.

### Detect stolen credentials and ATOs

Use risk scoring to block compromised accounts, stolen payment methods, and payout changes before funds move.

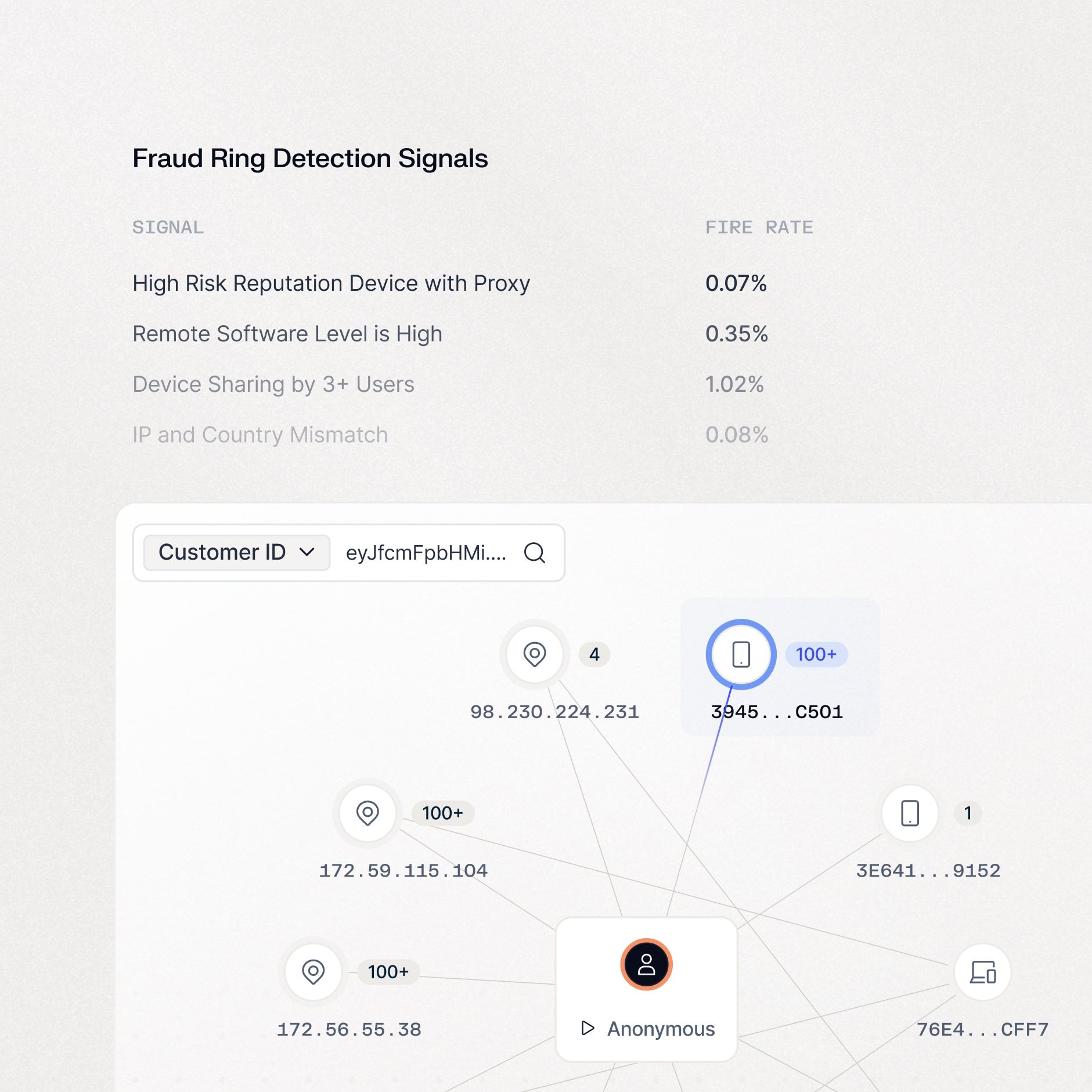

### Uncover fraud rings and collusion

Identify shared infrastructure, synthetic identities, and payout manipulation linking buyers, sellers, and mules.

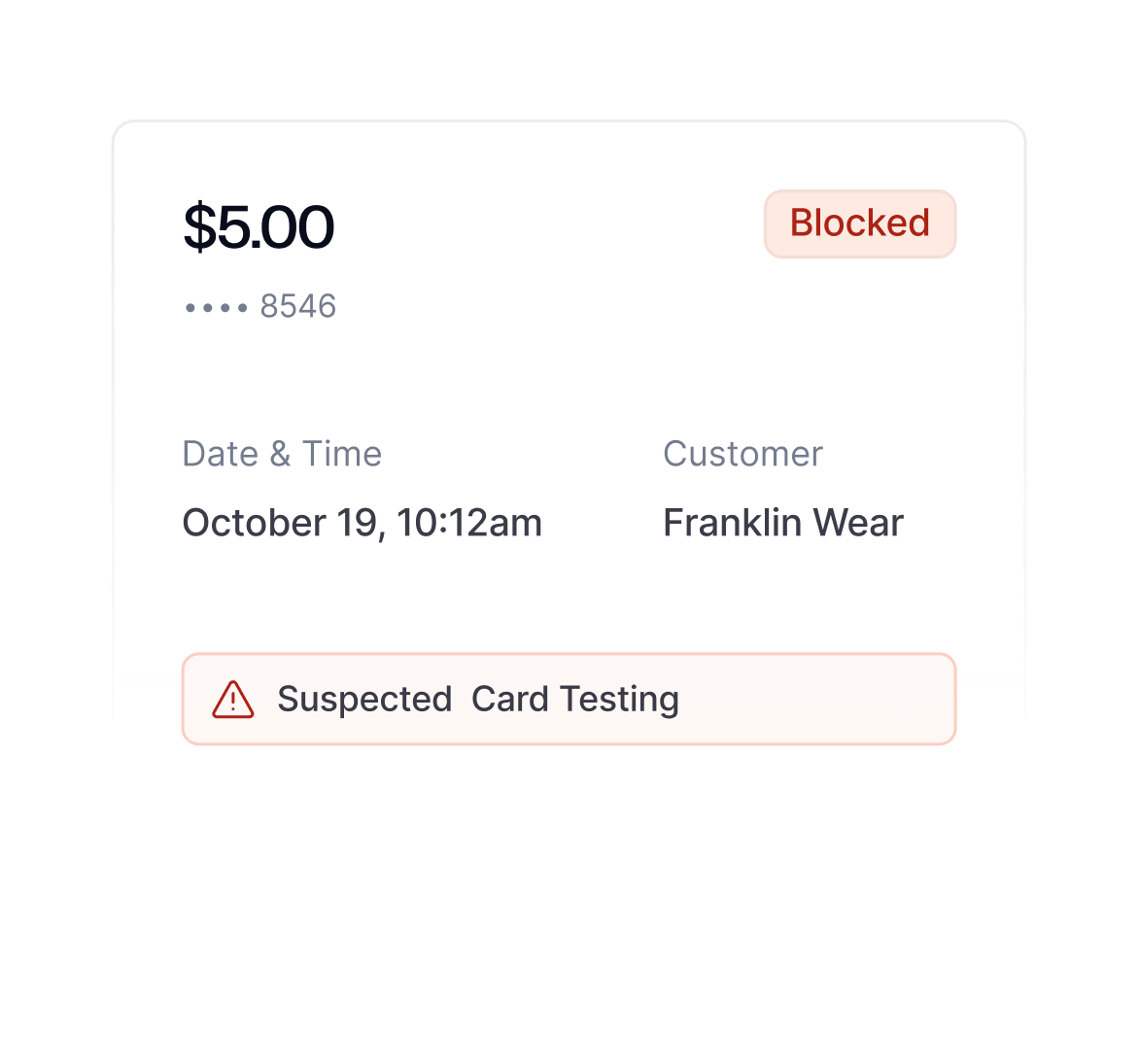

### Stop card testing before it triggers VAMP thresholds

Detect low-value probing attempts, authorization sequences, and multi-merchant card testing patterns that inflate dispute ratios and put your Visa acceptance at risk.

## Gift cards and digital goods

Digital Goods Fraud

Stop stolen funds before they convert into gift cards, crypto, or other liquid digital assets.

### Prevent stolen payment monetization

Block stolen cards, stored credentials, and virtual cards used to instantly purchase convertible digital goods before disputes surface.

### Stop card testing and burst purchase attacks

Detect low-dollar probing, micro-transaction abuse, and bot-driven bursts across SKUs with velocity monitoring at the account and device level.

### Block automated bulk abuse with digital-native signals

Identify scripts targeting limited drops and arbitrage-prone SKUs using device, identity, session, and value-extraction signals.

## Digital wallets and iGaming

In-App Purchase Fraud

Control deposit and cashout risk without disrupting legitimate play.

### Prevent stolen payment funding

Block deposits made with compromised cards or bank credentials, including high-velocity payment method switching on new or recently accessed accounts.

### Disrupt deposit-to-cashout abuse

Catch bonus harvesting, layering sequences, and mule activity across wallet behavior and withdrawal destinations.

### Stop ATO and automated funding attacks

Surface credential stuffing, bot-driven logins, and rapid account takeovers before illicit transfers clear.

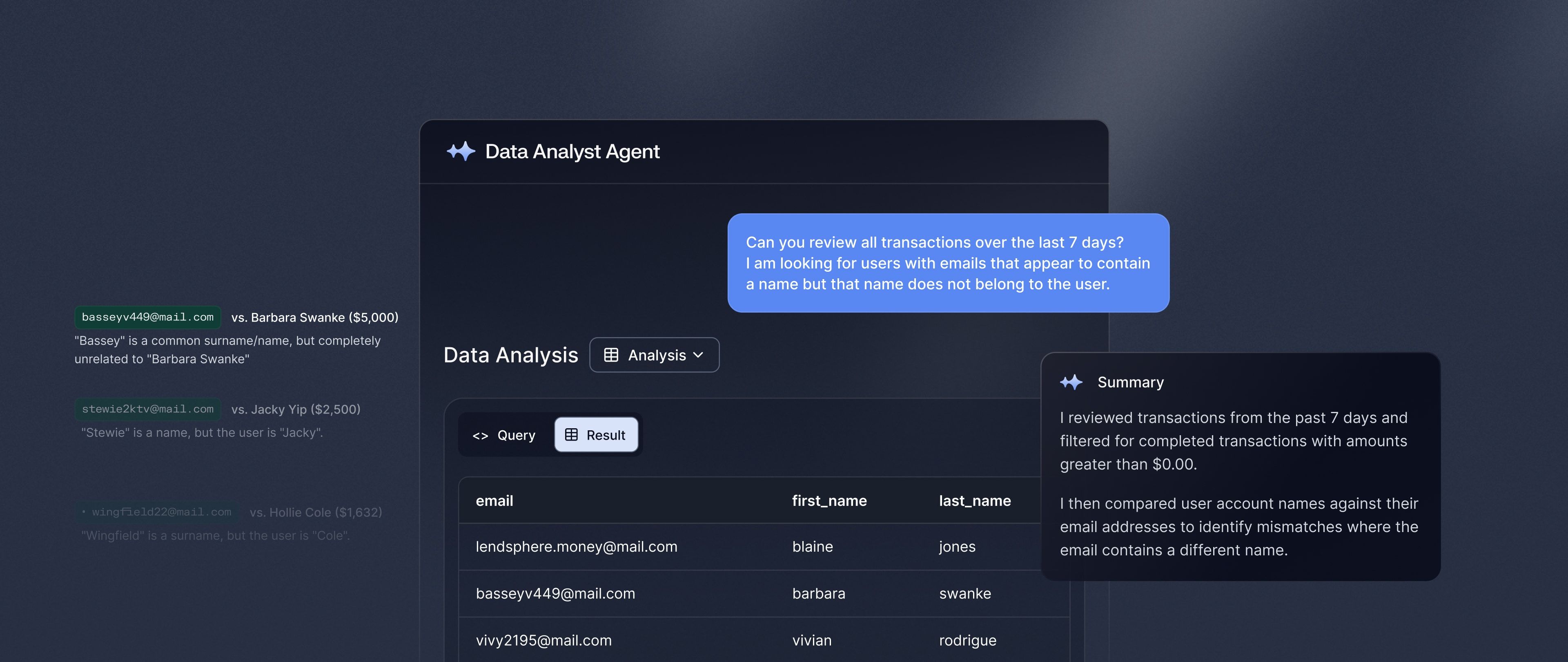

## AI agents built for fraud operations

Complete deep analysis in minutes, fine-tune fraud monitoring rules, respond to new attacks, and automate dispute filing.

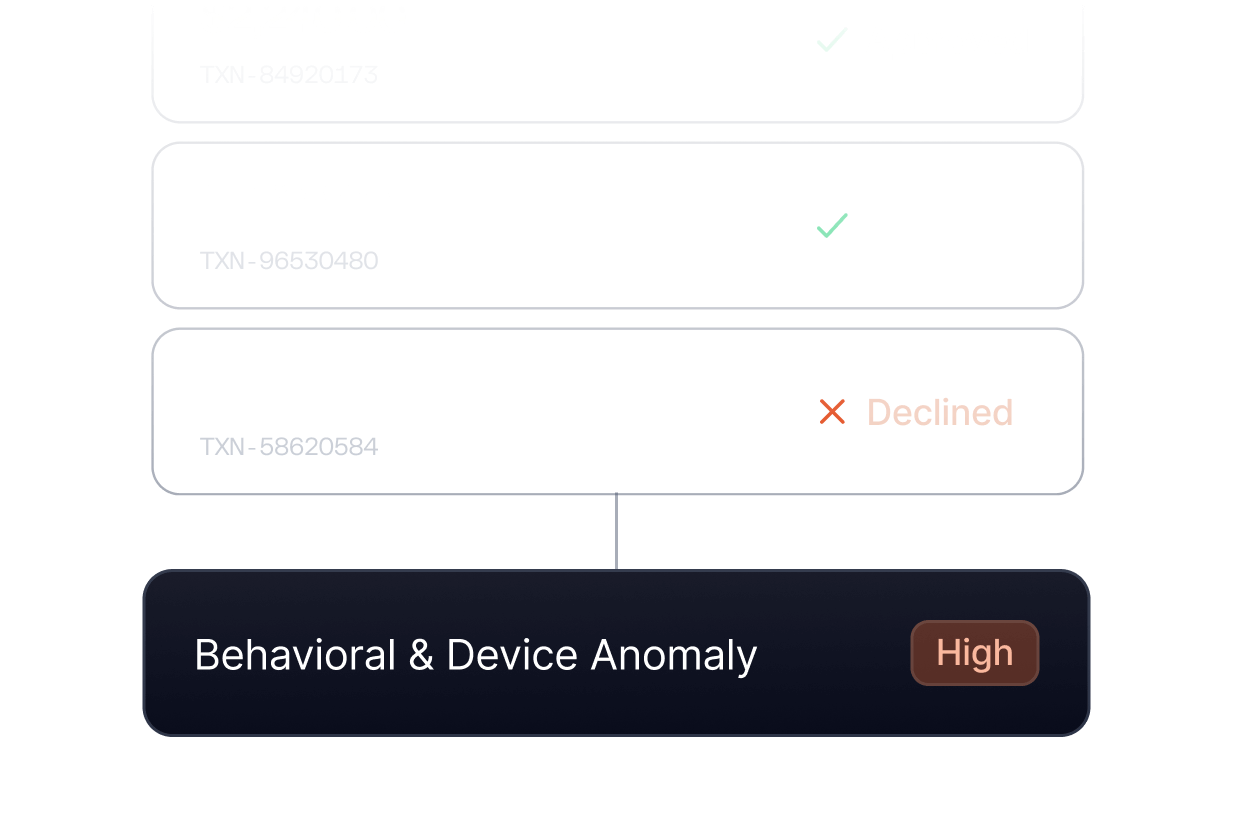

### Continuously analyze transaction behavior and payment anomalies to detect unusual velocity, merchant patterns, or repeat disputes.

### Investigate shared identifiers across users and payments, including common devices, IPs, emails, and cards linked to coordinated abuse.

### Generate and recommend anomaly-driven rules based on emerging fraud patterns and transaction outliers.

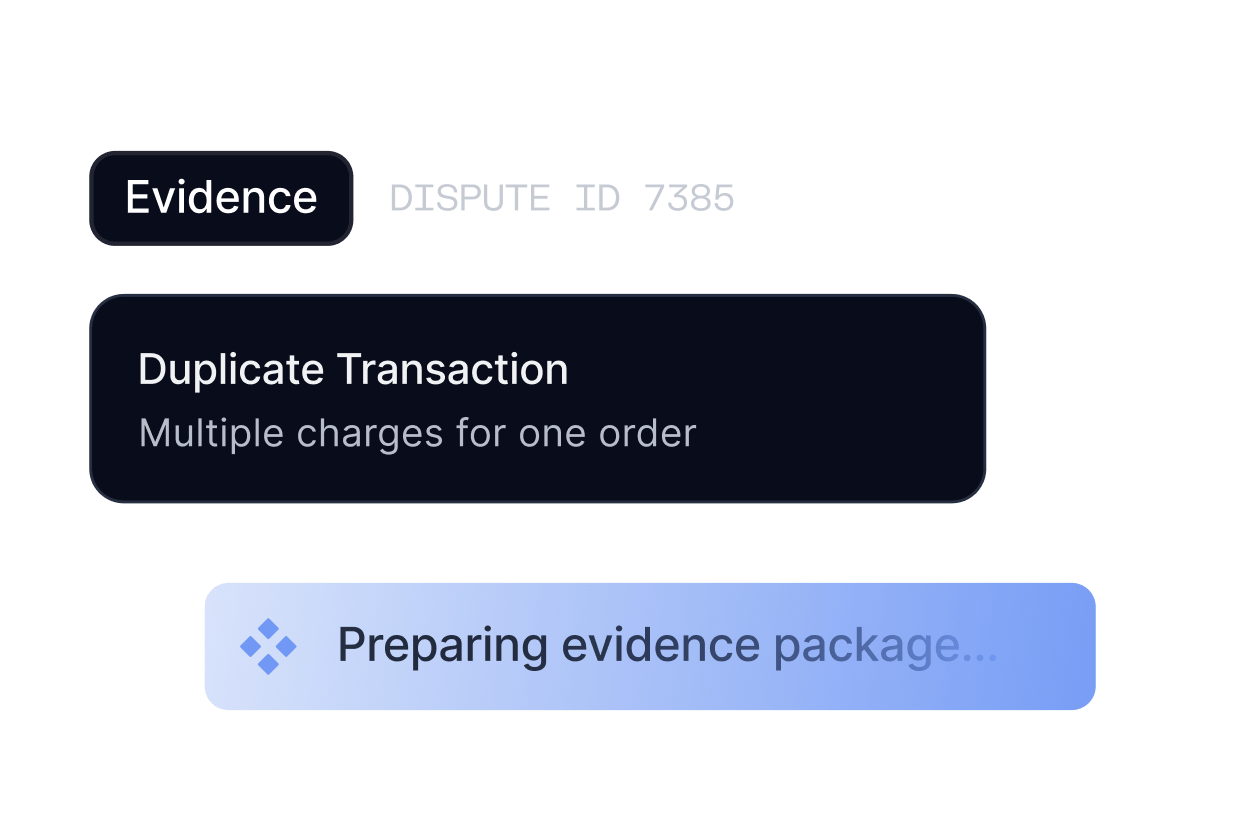

### Automatically assemble and file disputes with explainable documentation.

## Recognized by Nacha for ACH payment risk

Sardine is a Nacha Preferred Partner for Fraud Prevention, Risk and Compliance, supporting PSPs and acquirers with bank-grade ACH controls aligned to Nacha operating rules.

## Built for modern payment fraud operations

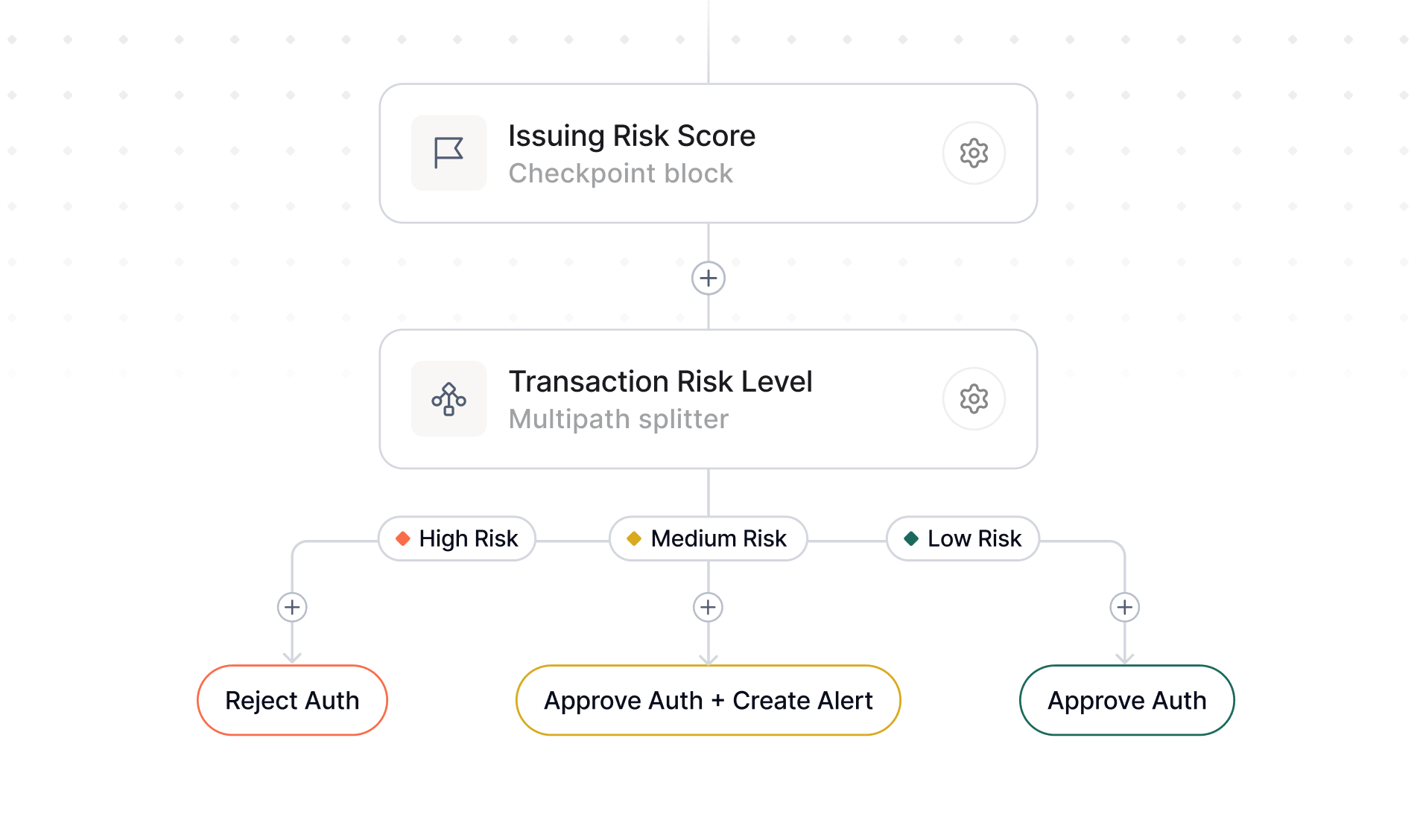

### Turn risk signals into action

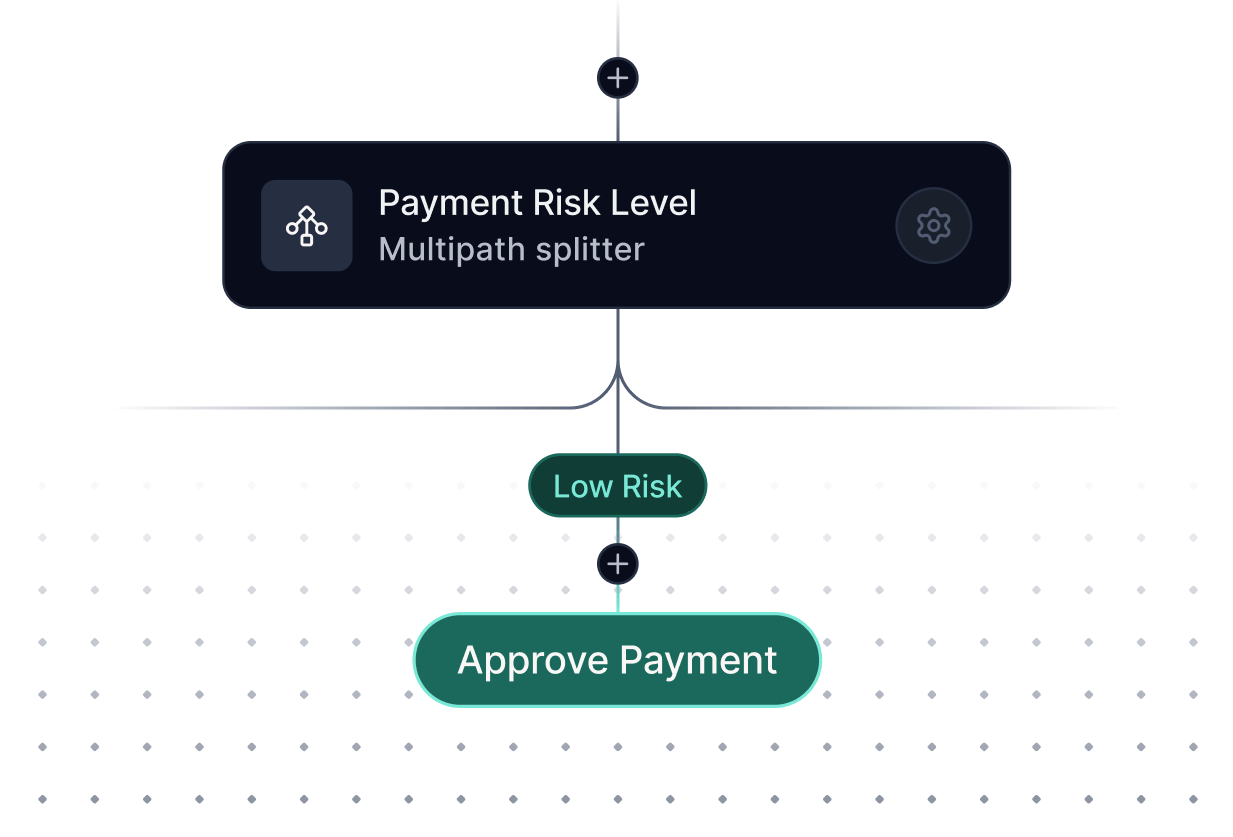

Create and deploy your own rules that control approvals, step-ups, holds, disputes, and payouts across rails

Rules & Workflows

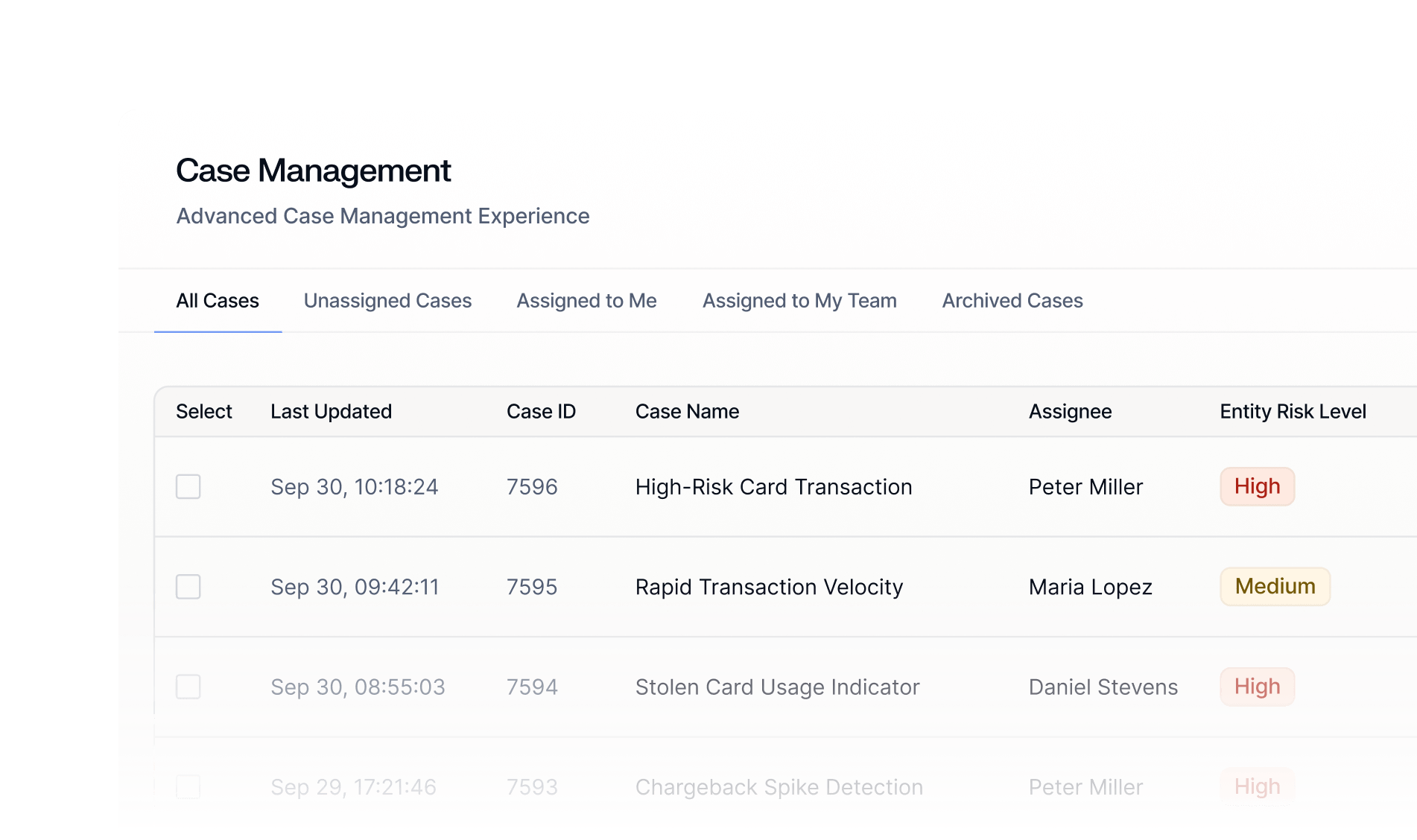

### Resolve payments end-to-end

Review payments, perform investigations, manage disputes, and automate decisioning in one platform.

Case Management

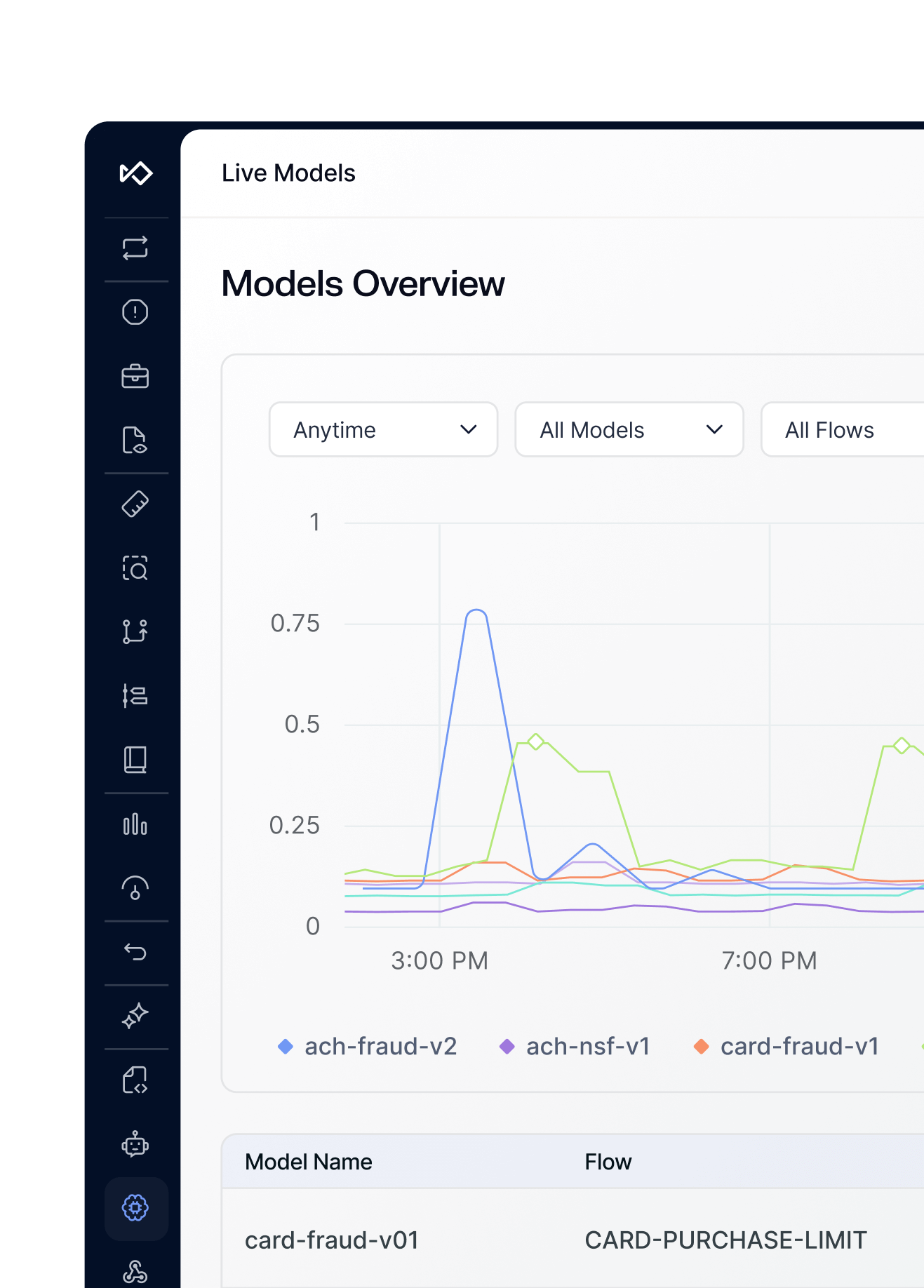

### Adaptive risk scoring

Score every payment in real-time using models trained on identity, device, behavior, and transaction history.

## Reduce fraud while increasing approvals

## Protect more

than just payments

Payments are one part of the risk lifecycle. Extend protection across onboarding, funding, and account activity.

### Identity Verification

Confirm identities before payment activity begins.

### Bank Verification

Validate funding sources and reduce ACH and payout risk.

### Credit Risk

Assess risk before extending credit or approving merchants.

## Frequently asked questions

### How does Sardine make payment decisions in real-time?

Sardine evaluates every payment inline using a unified decision engine that separates risk assessment from enforcement. Machine learning models score transactions using identity, device, behavioral, account, and historical outcome signals. Configurable workflows then translate that risk into precise actions within milliseconds, delivering consistent, explainable decisions across payment rails.

### How does Sardine improve authorization and SCA pass through rates without increasing fraud exposure?

Sardine identifies low risk transactions early and routes them through exemptions or low friction paths, while reserving step ups for elevated risk scenarios. This targeted enforcement approach reduces unnecessary challenges, protects approval rates, and keeps merchants within scheme and regulatory thresholds without relying on blanket controls.

### How are disputes and chargebacks managed alongside real time fraud decisions?

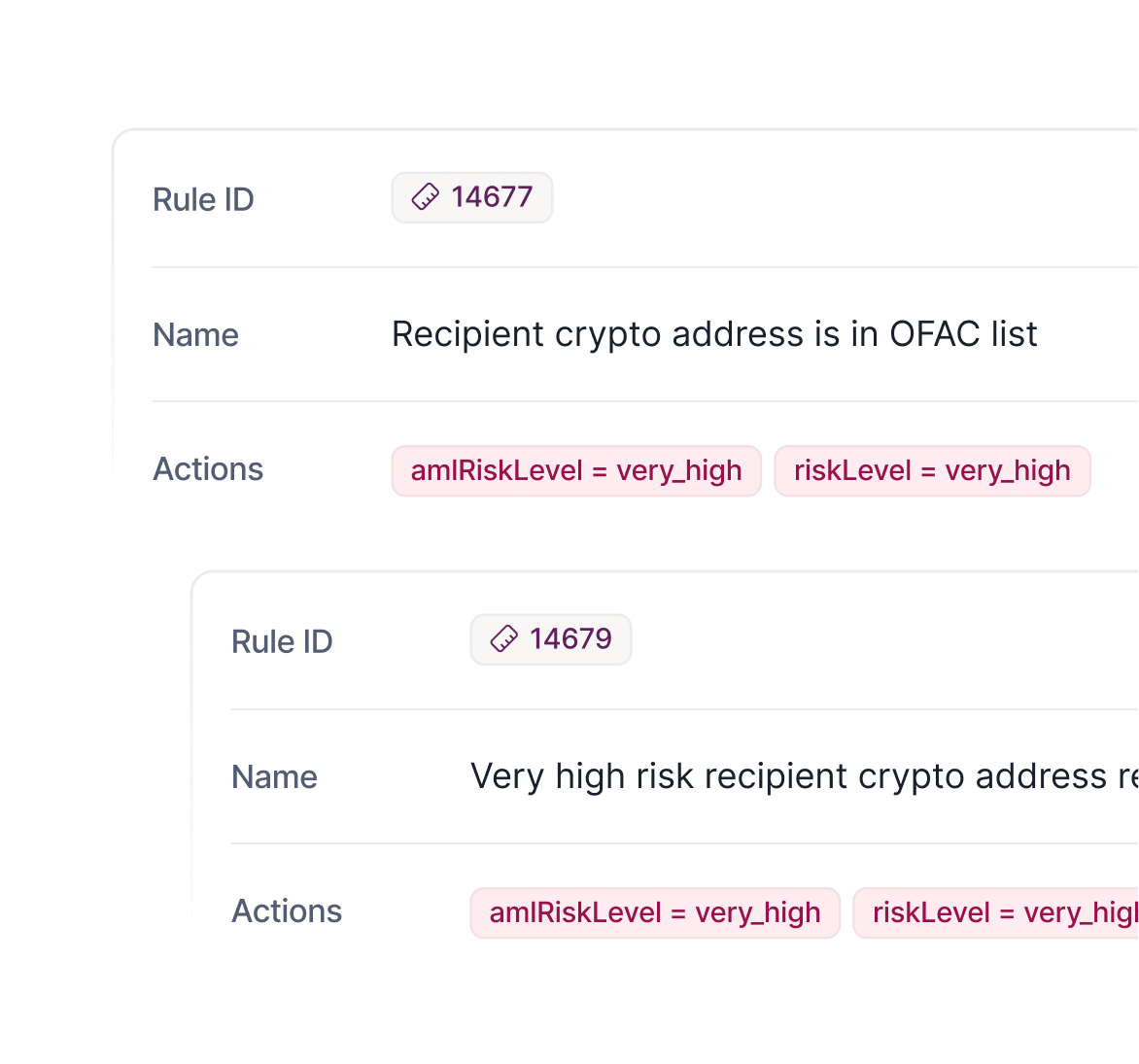

Disputes are managed within the same platform used for fraud decisioning, ensuring a continuous risk lifecycle. Evidence is automatically assembled from transaction data, device intelligence, behavioral signals, and delivery or access records. Disputes are structured by reason code, submitted in network ready formats, and tracked through outcomes to improve recovery rates and audit readiness.

### How does Sardine reduce risk on irreversible or delayed payment rails like ACH and RTP?

For rails without chargeback protection, Sardine shifts risk management earlier in the payment flow. Transactions are evaluated pre submission using account behavior, identity changes, and network intelligence. Based on risk, workflows apply controls such as holds, limits, delayed releases, or re verification to reduce exposure before funds move or settle.

### How does Sardine help teams respond to fraud spikes or emerging attack patterns?

Sardine combines real time anomaly detection with operator controlled workflows. When behavioral patterns or fraud rates shift, teams can immediately adjust thresholds, controls, or enforcement strategies without engineering involvement. Models continue learning from outcomes, while workflows provide fast, explicit control during live incidents.

### How does Sardine ensure decisions remain explainable and auditable at scale?

Every decision includes structured reason codes and feature level insights that show why an action was taken. This transparency supports internal reviews, regulatory requirements, partner audits, and continuous optimization across fraud, payments, and compliance teams.

### How does Sardine balance automation with human oversight?

Automation handles high volume, low ambiguity decisions, while complex or anomalous cases are routed into configurable review queues. This hybrid approach reduces operational burden without sacrificing control, allowing teams to focus human effort where it has the highest impact.